Constellation Software - Two Strong FCF Catalysts in 2024

Breaking down underlying free cash flow drivers

At the end of last year, we published an introductory article on serial acquirers and how their acquisitive rinse-and-repeat strategy influences expected shareholders returns. Go check it out, if you haven’t already.

When relying on stock screeners, chances are that serial acquirers like Lifco, Indutrade, Constellation Software, Topicus.com won’t make the cut to receive the compounding quality label. At least, at first sight… That’s precisely why we don’t use stock screeners to base our decisions on.

Whether it’s share-based compensation, one-offs, unclear net debt calculations, screeners are a flawed way of analyzing and defining your investable universe. We rely solely on company filings, management interviews and fundamentally relevant information.

Two reasons that may come to mind as to why serial acquirers tend to be treated differently by investors:

lower net income due to high amortization non-cash charges on acquisition-related intangibles (i.e. the purchase price accounting method causes the newly created/activated value of trademarks, clientele network et cetera of the acquired subsidiary to be amortized over an 7-10y period).

debt structure: financial debt, outstanding put-call considerations, leasing.

and as a bonus: several special cases related to minority interests and preferred convertible shares; all of which are relevant must-knows for shareholders in Constellation Software and its spin-out companies Topicus and Lumine.

In this piece, we’re going to take a closer look at how Constellation Software’s income and cash flow statement should be interpreted, in order to lay the foundation for an objective valuation assessment and pencil in realistic expectations. Over the past months, we’ve received multiple questions from clients ranging from “how to value CSI?” to “how should we look at the free cash flow available to shareholders (FCFA2S) related to the two spin-outs?”

Non-Cash Items and Non-Controlling Interests

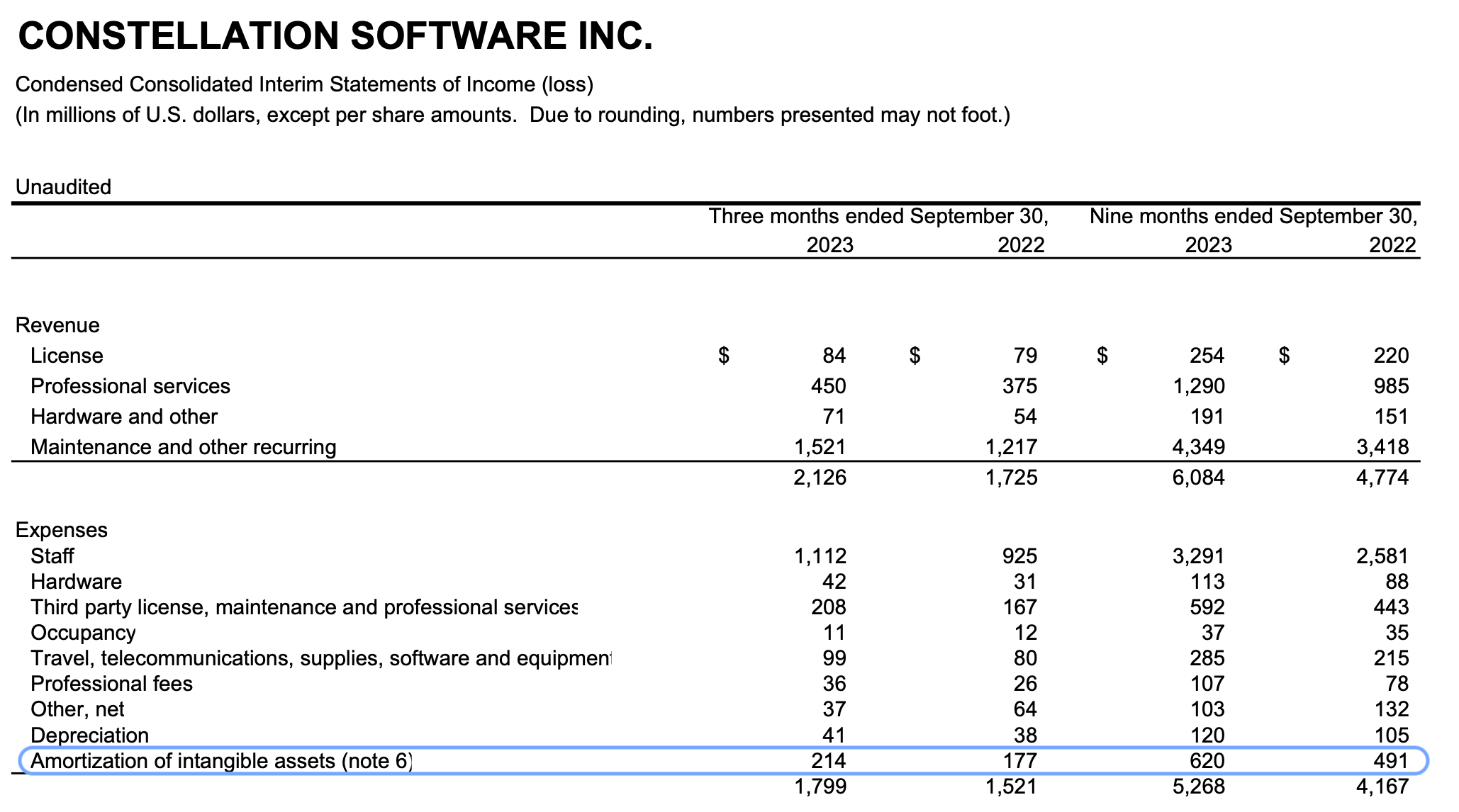

Let’s start off by sorting through the income statement and elements that could have distorted the overall trend. For simplicity sake, we took CSI’s latest Q3 2023 figures and highlighted the main “to-be-discussed” items.

Amortization of intangible assets: this is a common non-cash element for serial acquirers and even more so for Constellation Software. Typically, acquired intangibles are amortized at 10% to 13% per annum. Some might be skeptical about the high relative weight of these non-cash charges in CSI’s total expenses but we believe the useful life of its intangibles to be much longer than 8-10 years. After all, VMS businesses are characterized by relatively low organic growth, sticky customer base, pricing power and end market constraints (e.g. one VMS business focuses solely on platform software for schools, another one on library tech solutions and so on). Remember that the bulk of CSI’s acquired entities have been around for multiple decades already. If CSI were to stop completing acquisitions, the amortization charges would eventually dry up, thereby improving the reported EBIT.

The IRGA/TSS membership liability revaluation charge: going back a couple of years, Constellation Software acquired TSS at the end of 2013 with the seller, Joday Group, retaining a minority stake (33.29%). The agreement between CSI and Joday on governance (appointing executives) and various call-put exercise scenarios was formalized through the TSS membership liability. Due to CSI’s 100% retention of TSS’ free cash flow and the agreement being recognized under IFRS, CSI has since registered the “cost” of including TSS’ free cash flow that belongs to Joday. The quarterly revaluation of that liability is driven primarily by growth in recurring maintenance revenues. Still, these IRGA revaluations are non-cash charges. In 2021, TSS and Topicus (or Topicus.com BV) completed their merger, which led to the termination of the TSS membership agreement and the creation of a new one called the IRGA between CSI, Joday and IJssel. The latter refers to the Topicus sellers who reinvested roughly 25% of the proceeds back into the newly formed entity. Prior to the merger and subsequent spin-out of CSI’s exchanged subordinate shares, CSI and Joday Group went ahead with a corporate reorganization and dividend payout.

Redeemable preferred securities expense: as a result of the Lumine spinout, preferred and special shares were issued to CSI and the WideOrbit vendors. Long story short, there’s a dividend payment attached to these shares (payable on March 24, 2024). More importantly, one year after trading started in the spun out Lumine shares, the aforementioned parties will face the choice of getting paid in cash (by Lumine) or converting their shares into ordinary/subordinate voting Lumine shares. Just like with Topicus.com, conversion into ordinary shares will again make CSI a direct Lumine shareholder.

Non-controlling interests:

As of today, Joday and IJssel collectively now own a 39.7% minority stake in Topicus Coop. Under the IRGA and as required by IFRS, the combined share count held by Joday and CSI is Constellation Software’s total controlling interest. Because of the prior TSS membership agreement and thus Joday’s already existing stake in Topicus Coop through the TSS minority stake, the Topicus.com spin-out actually never resulted in CSI having a 0% controlling interest. CSI’s direct ownership in Topicus Coop currently stands at 30.35% but it hasn’t always been like this. Additionally, there are NCI in some of Topicus’ Coop fully-consolidated subsidiaries, such as Signity (27.3%), to which we’ll have to make free cash flow corrections.

The Lumine spin-out is a slightly different story with the non-existence of IRGA:

1 super-voting share held by CSI, i.e. Lumine being fully consolidated into CSI’s financials.

Just like with the Topicus.com spin-out: virtually all subordinate voting shares were distributed to CSI shareholders with the preferred shares being unconverted till March 25, 2024. So from a CSI shareholder perspective, Lumine’s NCI is now 100%.

As mentioned before, on March 24, 2024, the preferred and special shares will receive a one-time dividend. The upcoming Lumine dividend of approximately 60M USD for CSI won’t show up in CSI’s cash flow statement (Lumine is part of CSI’s consolidated scope due to the Super Voting share). However, the dividend payment related to the rollover group’s special securities will be subtracted from CSI’s total consolidated financing cash flow.

The devil is in the details: once the preferred shares are set to be converted into ordinary subordinate voting shares, CSI’s economic interest will increase at the expense of Lumine owners who aren’t CSI shareholders (anymore). Always keep the fully-diluted share count in mind for valuing the spin-out companies individually.

FCF Drivers in 2024

The income statement separates net income attributable to CSI shareholders from net income destined to non-controlling interests. However, this is irrelevant to the cash flow statement which sums up all cash flows, thereby neglecting the existence of NCI and CSI’s economic interest in the spin-out companies. (note: due to rounding, the below numbers may not foot).