Constellation Software's 2026 AGM

A 4-hour discussion on the past, capital allocation, AI, and what could be next

Last Friday, Constellation Software (CSI) and its spin-out companies hosted the annual general meeting in a hybrid format - for the first time in several years, allowing shareholders to ask questions live in-person. The AGM didn’t reveal any major surprises other than underscoring the collective expertise that spans the entire CSI leadership team, whether it be on product development, capital allocation (M&A and organic growth), or humility on what may come next.

Our friend The Pursuit of Compounding already posted a free update on CSI’s AGM too, so give it a read as well:

Opening Remarks

Mark Miller started with:

I've been here for over 30 years and we've always been on a perpetual journey of learning. Every day you learn something new, and I've learned things just by listening to our business leaders and talking to my peers across Constellation. - Mark Miller, CSI’s CEO and President

Doing what’s worked well, CSI continues to stick to the decentralized structure, even as AI’s looming and should, according to others, require a standardized strategy to be on top of the latest developments:

There’s no CIO who decides what AI platform we use, or what we should do, or whether we should turn right or left or do this or that. That’s done by our business leaders across the world, and that helps us a lot because it lets us bring new companies on board that want to be part of this ecosystem and learn from this environment. But I want to make sure you understand this when you’re comparing us to other companies: we are very decentralized. We believe in this. We believe that our businesses all across the world - and as you can see, there’s hundreds and hundreds of them - are the ones that should be making the decisions. They’re the ones that are running each of those businesses, listening to their customers, and building their products. - Mark Miller

All of the above shouldn’t come as a surprise, and in our December 2024 write-up, we listed several of CSI’s top management’s quotes over the years.

Even two companies in the same city in the same country can have two very different cultures, and that’s okay. That’s important because one of the advantages of joining Constellation is we’re not here to change your culture. We’ll measure you—some of the events we ran used to have people wear their numbers on their name tags. You need to be measured if we’re going to trust you to run your business all over the world, but you should determine what your culture is and how that works, because that helps you address your customers better and solve problems they really need help with. - Mark Miller

Evolution Over Revolution

While CSI’s been constantly evolving, we argue there’s no complete revolution needed to drive the next chapter of market-beating (>12% per annum) performance over the next decade. It’s about capital deployment and the related immediate ROIIC, supported by acquiring small businesses frequently. It’s more about doing what’s worked (so) well and executing on initiatives where the math makes sense.

There's no way you could say back then that this was the plan; we probably thought we'd have fewer, larger businesses. But we've learned that having small businesses - and our businesses are small, a lot of them have dozens of people with a few hundred customers, sometimes less - is the way to go. It turns out, and I'm going to talk a little bit more about AI in a bit, it's actually positioned us very well because we are right there with the customers helping them as they deal with changes in their businesses through time. - Mark Miller

When constructing a valuation model, it’s more about understanding what it’ll take to grow earnings in the low- to mid-teens percent. In doing so, one’s likely to conclude that there isn’t much M&A scaling required, as we’ve shared in the Q1 recap (and in prior quarterly reviews). Obviously, 12-15% per annum growth isn’t anywhere near the last three decades’ performance but that shouldn’t be part of the discussion, in our opinion.

Sounds very obvious but with the recent months’ share price performance, the feeling we’ve got is that increasingly more shareholders are asking for a massive overhaul in, e.g., investor communication, beefing up capital deployment, and generally, doing things to turn around short-term momentum. Simply stated, the stock’s down so management should fix “it”.

Late December 2024, we were hosted on the Capital Compounders Show to talk about CSI and other quality companies. Frankly speaking, aside from the share price volatility, the AI narrative, and the fact that CSI’s scale (and challenging comparison base) has grown again, very little’s changed.

Looking at the recent financial performance, the discussion on the reinvestment opportunity (quarterly volatility in M&A dealmaking) and organic growth is still here and has been for years.

What we’ve observed at CSI over the years is evolution over revolution. Think of:

the greater appetite for larger M&A (TSS, Altera, Optimal Blue);

being courageous to drop the hurdle rate for these (resulting a declining ROIC which is NOT an issue as long as you keep deploying capital at highly competitive returns (competitive as in: capital allocation that’s not to be found easily anywhere else);

developing the spin-out strategy (Lumine and Topicus, and most likely new names coming such as Modaxo);

VMS ventures, an;

lately, the PEMS. Moving from privately acquired to publicly listed entities with different dynamics and set of expectations.

The core principles have remained largely unchanged: there are well-defined hurdle rates for acquisitions, and the bonus scheme is driven by ROIC and growth. Having a low ROIC while pursuing growth will result in increased leverage, and given that the future is inherently unknown, the optimal level of leverage isn’t always easy to determine beforehand.

Share Price vs. Fundamental Momentum

For us, shareholder returns are the outcome of splendidly consistent performance and agility that builds over time, coupled with rational executives. We invest in companies that are led by managers who reflect our own perspective on business management and capital allocation.

In the past, we were very math-oriented but the quantitative aspects of corporate culture are equally (if not more) important. “If you don’t trust the people, don’t do the deal.” Our excellent executives are not focused on gimmicks but performance that’s driven by a couple of time-tested criteria.

What we value about CSI’s leadership is the simplicity/effectiveness in explaining concepts. Mark Miller’s comments on AI - spending and business vulnerability illustrate this:

I prefer organic growth, return on invested capital, and hard numbers you can really wrap your head around because those are metrics you can truly trust. But I'm not saying people shouldn't use those assessment tools if they find value in them. Ultimately, your weak businesses will stay weak if they aren't led by the right people.

The share price will most likely not reflect ongoing progress in real-time. And once executives doing the right thing start feeling the pressure to accelerate growth by making rash decisions, it might end up attracting the wrong shareholders.

In a recent interview, CFO Baksh said that he was happy to buy more shares of CSI (through his cash bonus) at lower prices, though he didn’t put it like this: “Our stock is so massively under-priced and we’ll (have to) do something about it.”

That’s radically different from the short-termism and egregious options packages you’ll find in other high-growth places… There, executives will be pumping expectations so that the options do not expire worthless. In a raging bull market, conservatism/realism does not pay off but we’re not invested to cash out in a bull market and time the next downturn. We cannot time inflection points; we simply seek to survive the whole cycle and make a satisfying return over the long haul.

Companies should avoid attracting short-term investors who look for near-term catalysts no matter what the long-term economic consequences, oftentimes leading to permanent destruction of long-term shareholder value as managers fail to focus on the drivers of real value. It’s what we’ve talked about in a previous (free) blog.

Needless to say that, in the end, we all want to earn solid returns on our equity investments but the timing and magnitude is tough to predict. Many investors fail because they’re uncomfortable with the uncertainty around when and how much a stock will return.

Growth in earnings may be quite linear to some extent (off note, since the launch of the Substack newsletter, our portfolio delivered +13% growth annually in underlying earnings per share). Share price momentum, on the other hand, will vary due to investor expectations and thus interest in the company-specific equity story. Today, investors are bullish on the AI trend and quite bearish on more discretionary consumer goods and software companies, as evidenced by the latter’s dismal share price performance and increased short selling.

However, momentum cuts both ways - when the last buyer’s just stepped in, who’s gonna sustain upward momentum from here? Conversely, if relative value is attractive (a reasonable valuation multiple and strong or potentially accelerating growth), intrinsic investors should eventually show up - provided they’re in a position to do so (active vs. passive investing).

Many investors aren’t able to think long term anymore, which has some serious implications on price discovery and the forward relative performance in crowded versus less crowded assets. Being patient investors, we focus solely on long-term fundamental momentum and let smart capital allocators do the heavy lifting for us. Over time, value will eventually out.

Verticals as a Tool to Structure Acquisitions

Turning back to CSI’s AGM, one of the themes was on verticalization, which is a great way to structure and increase the odds of success for acquisitions. If you’re a group of different companies, say predominantly healthcare related, and a finance related business for sale pops up, it’s harder to pitch yourself.

By grouping your acquisition prospects into separate verticals and creating subsegments within one operating group, you can run the M&A playbook much more effectively, and you build a direct reputation of being the preferred forever home for businesses. One of those verticals within the CSI group is Modaxo, which resembles transportation related VMS.

We've got 41 businesses today in Modaxo across all different functions in every department of transit operations around the world. What this lets us do is build a layer above that which Modaxo can invest in. We still give federated control to the underlying businesses, but we're able to build a platform that allows a transit authority to start asking questions and building actions and agents that ignore all the industry, underlying business, and product boundaries, looking at it from an ecosystem perspective. I think we're in a position that none of our competitors are in in that regard. From a Modaxo perspective, that's an investment that we're making that each of our businesses will be able to leverage, and the feedback we're getting from the industry is that they're sort of blown away by this approach. We're looking forward to seeing that really build out in the coming months. - Bill Delaney, CEO of Modaxo

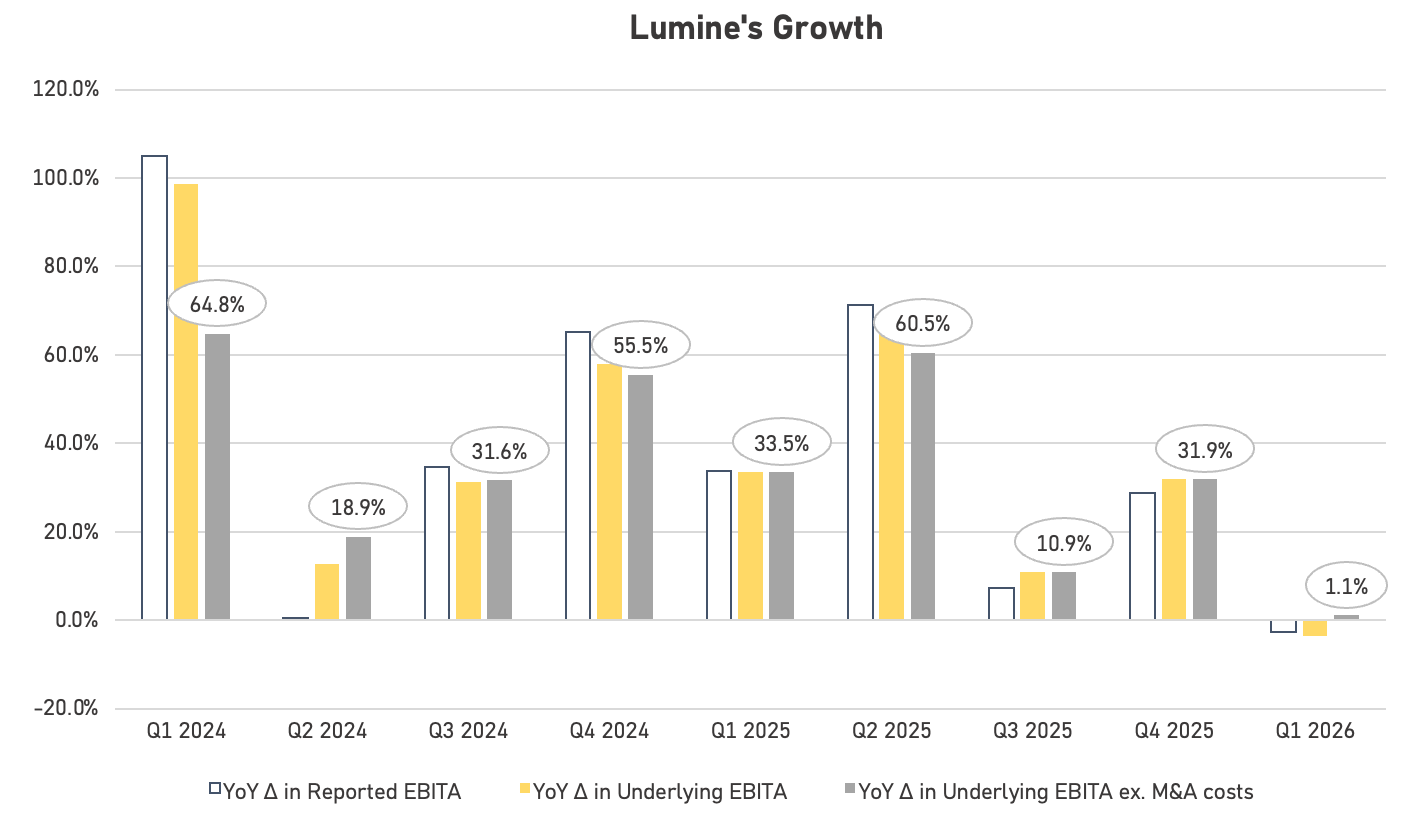

The same’s true for Lumine. While it seems to be the most sector-constraint publicly-listed option (compared to Constellation Software and Topicus.com), its very deep understanding of the telecommunications space allows for a swift integration of acquisitions. Nyland remains very upbeat about the M&A pipeline and the relative positioning of Lumine compared to other acquirers.

We really see that there are three strategic acquirers in our space ultimately, and every other business in this industry is in a transient ownership position, whether it's strategic, private equity, or even founder-run businesses. The final destination needs to be one of the three of us, and we're just the exciting, interesting alternative to a functional integration, synergy-based model. Customers really like our model, so they're going to steer these companies towards us over the next 5, 10, or 15 years, and that really excites me about what size business we will ultimately build. The adjacencies around our markets are very significant as well, so we're very, very excited about the future.

As highlighted in the Q1 recap, the recent quarter was atypical due to some project timing and closing the Synchronoss deal but that should be fixed soon.

Artificial Intelligence - Specific Use Cases

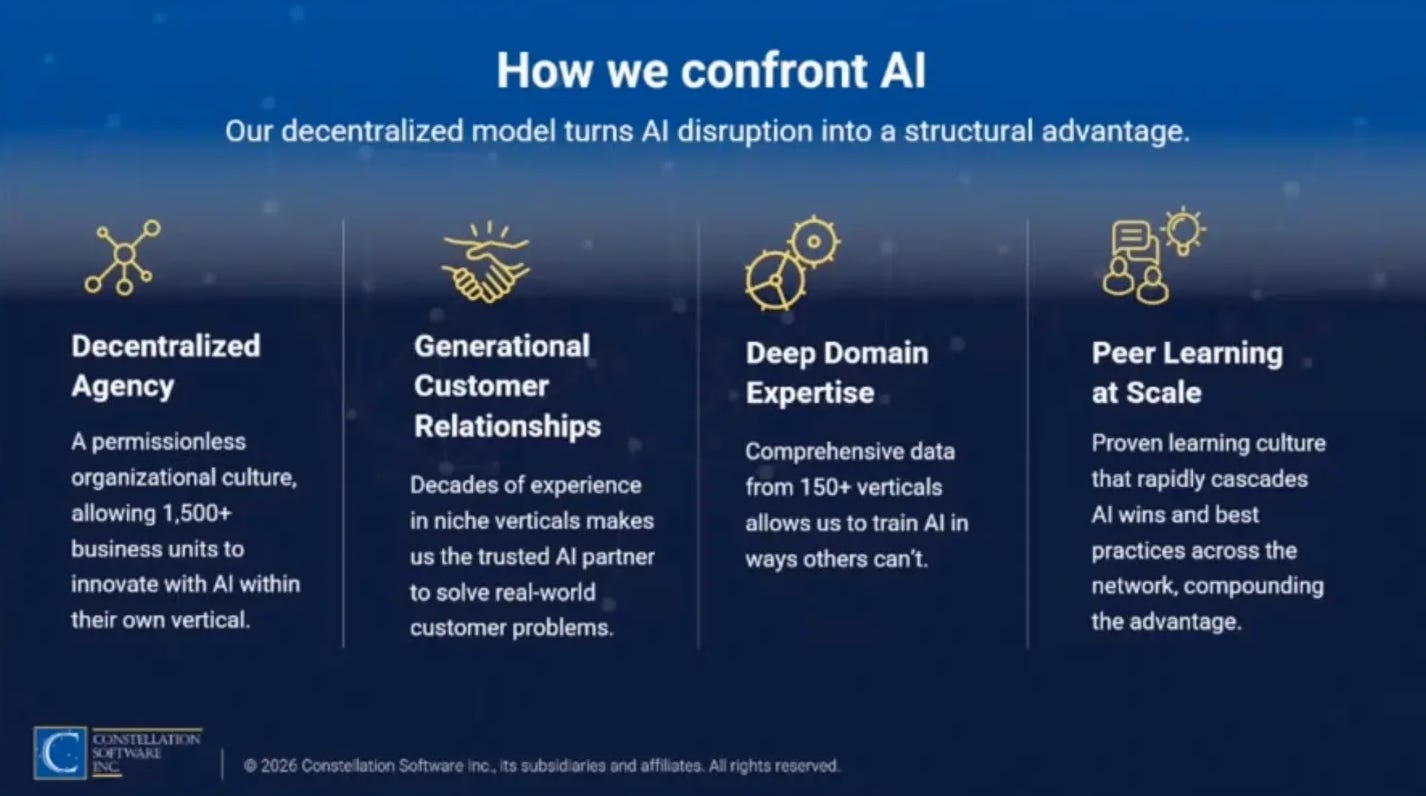

AI also fits into the verticalization strategy. The better you understand the precious data and workflows, the more you’ll be able to leverage their value and help your customers out. When clients value your offering, you’ll end up in a situation where being decentralized offers you flexibility and the wisdom of crowds versus a centralized structure where one management team can screw things up.

Think of fashionable consumer-related businesses that endured irreversible brand erosion. Oftentimes lying at the root of the problem: a wide gap between the top-level management team and day-to-day operators connecting with the customers. Know your customer.

We really believe in long-term relationships that are trusted with our customers, and we know the customer space. It isn’t a ChatGPT “go ask a question” type of situation - again, great product, but you have to know a lot in order to build products for customers. You’re dealing with trusted information. You heard from Santina that you’re dealing with patient data in cases like that; that’s valuable data and it’s got to be managed very carefully. But our biggest advantage, if you’re going to be decentralized, is that you’ve got to believe in peer learning. Our best leaders are the best at learning from each other, and it doesn’t matter how many decades they’ve worked for us, they’re always open to a new idea, a new way to do something, and listening to their customers. I really wanted to make sure you all understood this - it’s a question we’re asked about a lot, and our structure is our biggest advantage. - Mark Miller

AI should also help drive development times down.

If you think of a cycle time from concept through to production software, typically for us that was measured in months… And as we went through last year, we turned that into days. And today our cycle time is measured in hours. - David Nyland, CEO of Lumine

Andrew Jones, the general manager of Click Dimensions, talked about how they implement AI. As a horizontal marketing automation platform that provides outcome-based marketing solutions, Click Dimensions operates in a sector heavily impacted by AI advancements. The company’s leadership sought to leverage these technological shifts to transition from a horizontal service model to a vertical, transformation-driven approach.

The primary objective was to evolve the company’s existing chat and ticketing infrastructure. While traditional chat agents typically identify customer issues without resolving them, Click Dimensions aimed to develop a system focused on active problem resolution.

By utilizing the Constellation network of 1,500 companies for collaborative problem-solving, the organization worked to integrate AI into its framework to improve customer service mechanisms and drive business transformation.

It took us about four weeks to do it after going through those various steps. We launched it in January of 2026, and what we found was that in our customers’ interactions with this conversational agent, rather than being a lookup agent, it was a problem resolution agent. It effectively resolved 82% of all our tier-one tickets that went through the chat agent, which is fantastic. Most importantly, it allows us to generate greater customer intimacy because it means our humans, rather than having to waste time dealing with tier-one tickets, can spend time focused on tier-two and tier-three tickets, which are the most important things. Secondly, the time it took for a customer to get a problem resolved when it’s very simplistic became much faster. - Andrew Jones

Within the same panel discussion, David Wilkes who sold his business to CSI in 2018. At CSI, he oversees three/four business and attended a recent AI event from Harris. Coming back, they decided to completely rethink two subsidiaries’ offerings - Celcat (a timetabling software company in the UK) and Bullet:

Going back to the end of last year, our growth was running at about 12% per annum. Today it’s running at 23% per annum. Our vision is that we’ll double our revenues by 2029 - I think I’ve also been told I’m sandbagging on that. The interesting thing there is that growth is not driven by just going faster. It’s driven by us asking a totally different question: if we can go 50 times faster, what does that look like for our customers? For us, that meant we literally rebuilt our product from scratch. We reimagined what a new category of product might be. If you think about our old product, it was a system of record where you created, read, updated, and deleted data. Our new product is a system of action; it thinks, predicts, and gives you insights - it does really clever stuff for you. That creates huge value for our customers, and with value comes new price points, doesn’t it? With that, we are driving growth and seeing the results of that already.

Summing it all up, some pockets of CSI’s businesses will be affected by AI negatively; others are set to benefit but jury’s out on the magnitude of these changes. That’s quite simple to understand as CSI consists of >1,100 entities.

Net net, there isn’t much to be observed today.

I look at about 900 of the businesses, and I look at trending of organic growth, and I follow up with the operating group CFOs, etc., if there's anything that looks like an anomaly - and there are a couple things that might have popped out, and both of them had nothing to do with AI. - CFO Jamal Baksh

The bears could argue that this diversification makes it very opaque to assess the long-term risks to organic growth from AI. It’s quite similar to the discussion around attrition: when, why, and how do you lose customers? Within CSI, there are business units with 0% attrition (a payments wrapper is a nice tool to improve stickiness), and more horizontal segments that have to do a lot more to retain their clients. For that reason, each acquisition generates a different IRR. Nothing shocking.

As Robin van Poelje (Topicus) mentioned, it boils down to having the right people. In that regard, investing in CSI continues to be a bet on thousands of highly motivated and talented employees.

However, the way you approach the market and implement best practices differs, and it depends heavily on local management. I don't think that's always down to the country's culture; sometimes you get lucky with an acquisition that has fantastic people, and sometimes you don't and have to implement changes.

Furthermore, as it relates to AI, it may not even be high on the list in a customer-centric conversation. This is what Volaris CEO, Mike Dufton, shared:

Most of the engagement with the client is focused on the business users and what specific business problem we’re trying to solve. If AI ultimately is embedded in the solution, that’s not the opening conversation because the pace of technology, particularly as it relates to AI, is moving very quickly, and we’re often engaging with clients who are not necessarily even familiar with it. When we are dialoguing, we begin with the business challenge and how we think we can make them more efficient, rather than leading with, “Hey, we want to come and talk to you about AI.”

Capital Deployment

Finally, on capital deployment, CSI continues to look for all sorts of acquisitions as long as they meet the stringent return criteria. Whether it is for public or private deals, it’s got to make sense. We think that’s the main takeaway from the AGM: don’t expect the CSI team to throw good money after bad or loosen the disciplined approach to deploying capital.

As Bernie Anzarouth (Chief Investment Officer) replied:

Nearly always, when we've had the opportunity to bid on publicly traded companies that are for sale, they are working hand-in-hand with an investment banker that takes them out on a roadshow with a document and a confidential investment memo that talks about their business, and they do an appropriate job of scouring the world for buyers. Once that happens, you have to pay a premium over market to get that business. We're not in the business of paying up for these businesses in an auction; it just doesn't make sense for us.

This time, there were quite a bit of questions on the PEMS (Permanent Engaged Minority Shareholder) but as with many other capital allocation decisions from the past, it’s not CSI’s first rodeo.

I just wanted to say that 25 years ago, we used to buy minority stakes in public companies, and those companies ended up being put into play. It generated extremely high returns on our invested capital, but the average tenure of our investments was very short, and nearly 90% of the time we got outbid by a third party when the businesses were sold, which is sort of sad but understandable. That short-term activism was profitable, but it was a poor strategic fit with our objective of being good permanent holders of vertical market software businesses, so we stopped doing it. You can hear from the conversation today that we buy and hold forever for the long run, and PEMS is another tool. - Mark Miller

At the same time, PEMS is just one tool sitting in the box currently. More style drift, moving away from traditional VMS and buying 2-5 million USD businesses, could be in the cards.

So we are looking at other avenues. It's not just going to be software. Of course, the bulk of it is going to be software because that's what we're really good at and we've studied that over the last 30 years. You're going to continue to see a lot of that going forward, but there is a possibility of new stuff coming up. - CIO Anzarouth

Conclusion

Overall, we’d say the AGM didn’t contain any major surprises on how CSI’s being run. It’s business as usual. The reinvestment engine remains intact, and we fully stand by our assumptions shared in the Q1 recap. That’s our brief summary of what was a great AGM.

You can access the full video here.

Great recap, thanks for all these amazing quotes. I have to admit I didn't know they had already acquired minority stakes in publicly traded companies in the past... good to know. At the end of the day, as they also say, the only thing that can protect you in uncertain times like these is to have a great management team and great leaders. Let's hope it continues being the case for CSI!

Thank you for taking the time to review and share. It’s exciting to experience CSUs foray into public market opportunities. Perhaps it could consider acquiring http://DND.TO debt, and in collaboration with Engine, Blacksheep, Penderfund, Edgepoint and the Brethren, actualizng transformational value creation for http://DND.To