Dealing w/ Opportunity Costs As Quality Growth Investors

Contextualizing IRRs, optionality and relative performance

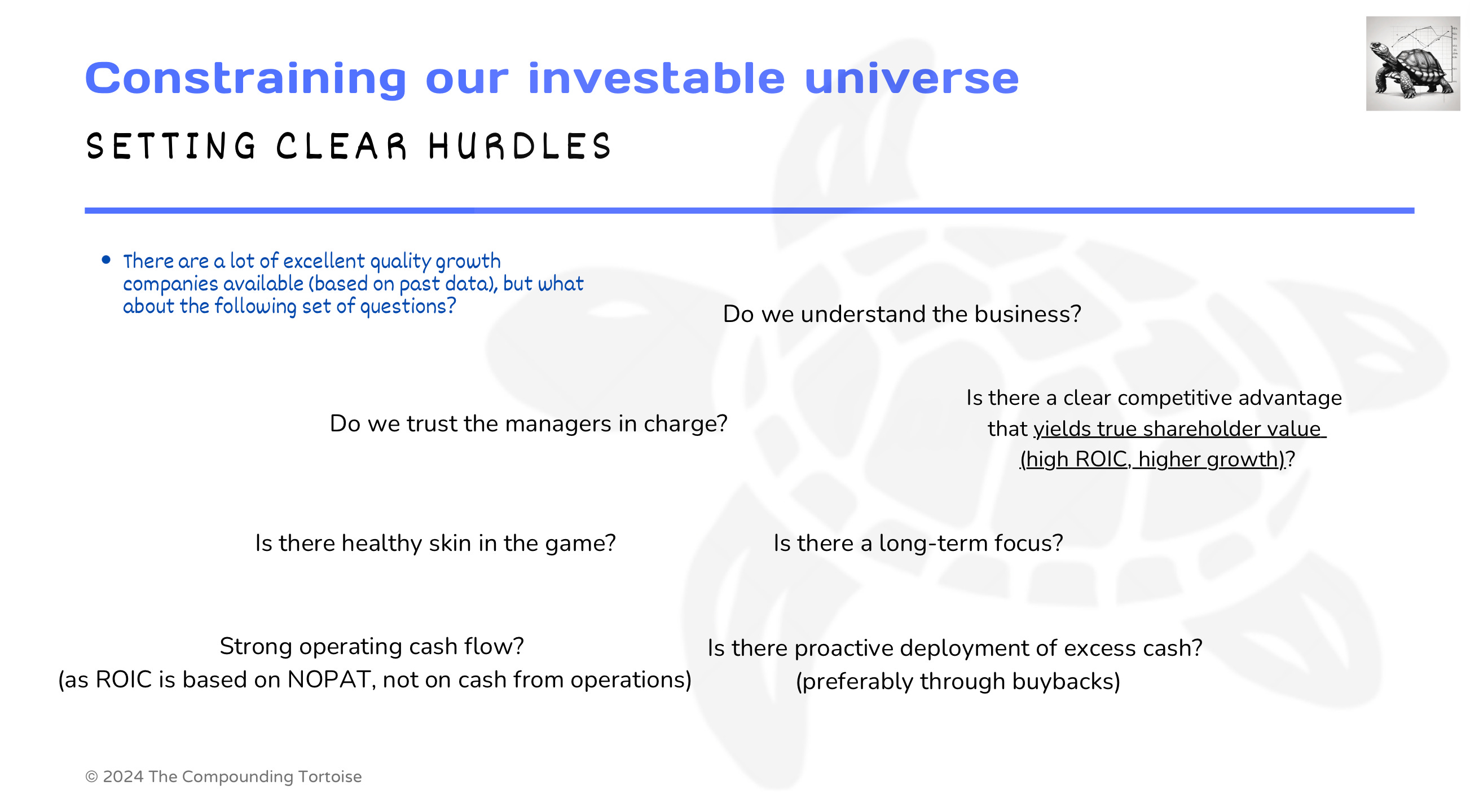

A quality growth investing strategy is highly unattractive from a relative risk perspective. Steady winners tend to underperform during a rising market environment, as we’ve highlighted in previous articles. In a bear market, they won’t make us money, and relative outperformance isn’t likely to make us feel any better (losing 20% when the market’s down 30%). On top of that, there are many possible quality investments, so we should set clear hurdles to separate the wheat from the chaff.

Aside from this, some of the best quality growth companies are trading at what many believe to be excessive multiples, but don’t necessarily see these revert. On the other hand, there are other well-priced quality compounders that could very well underperform our expectations over the next quarters, or even years.

That’s the opportunity cost active investors face: which stocks to pick, and what’s the likelihood of them outperforming the market? We argue that the quality growth investing’s outperformance relative to a benchmark is a by-product; it shouldn’t be our primary focus. Our goal should be to earn our targeted absolute return goal, whilst incurring a controlled amount of risk (i.e. low risk of permanent loss of capital).

At the same time, a market cap weighted ETF has now become an effective tool to better capture momentum/hype and multiple expansion for many tech companies. In short, there are several factors that make it harder for the average investor to stay the course.

Let’s address these topics a bit more in the below webinar (PDF material can be downloaded).