Diploma PLC

Sustainable quality compounding in action

Introduction

This new in-depth report covers the essentials of Diploma’s investment case and how the UK-based serial acquirer’s evolved from being a rather geographically constraint and slower-growing organization with “too high” ROICs into a diversified collector of structurally faster-growing businesses acquired at good to very good multiples.

Looking ahead for our subscribers - our next two in-depth reports will cover smaller-sized serial acquirers with little or no coverage on Substack. One of them is our recently pitched position. What do they have in common? Above-average organic growth and strong ROIICs on their acquisitions right from the start, oftentimes far ahead of the established names such as Lifco, Indutrade... Why do we want to cover them? Because researching those hidden gems is just an exciting brainteaser, and we’ve observed growing interest from our readers in unpacking the less obvious names - without lowering our hurdle for quality and attractive forward returns.

We’re also going to elaborate on some of the general pitfalls of the serial acquirer model, e.g., assessing financial metrics such as rolling ROIC. Interestingly, Diploma’s current management team is very well aware of these dynamics, allowing for a balanced approach to deploy capital at healthy returns commensurate with well-calculated risks, even as rolling return metrics were to come down due to the timing of M&A.

Consistent with our previously shared reports, one of the main objectives is to help our subscribers sift through reports more easily and build their own toolkit for analyzing businesses more confidently. The underpinnings of value creation and long-term shareholder returns, isolated from timing effects (luck), have been and will to continue to be consistent across time and geography.

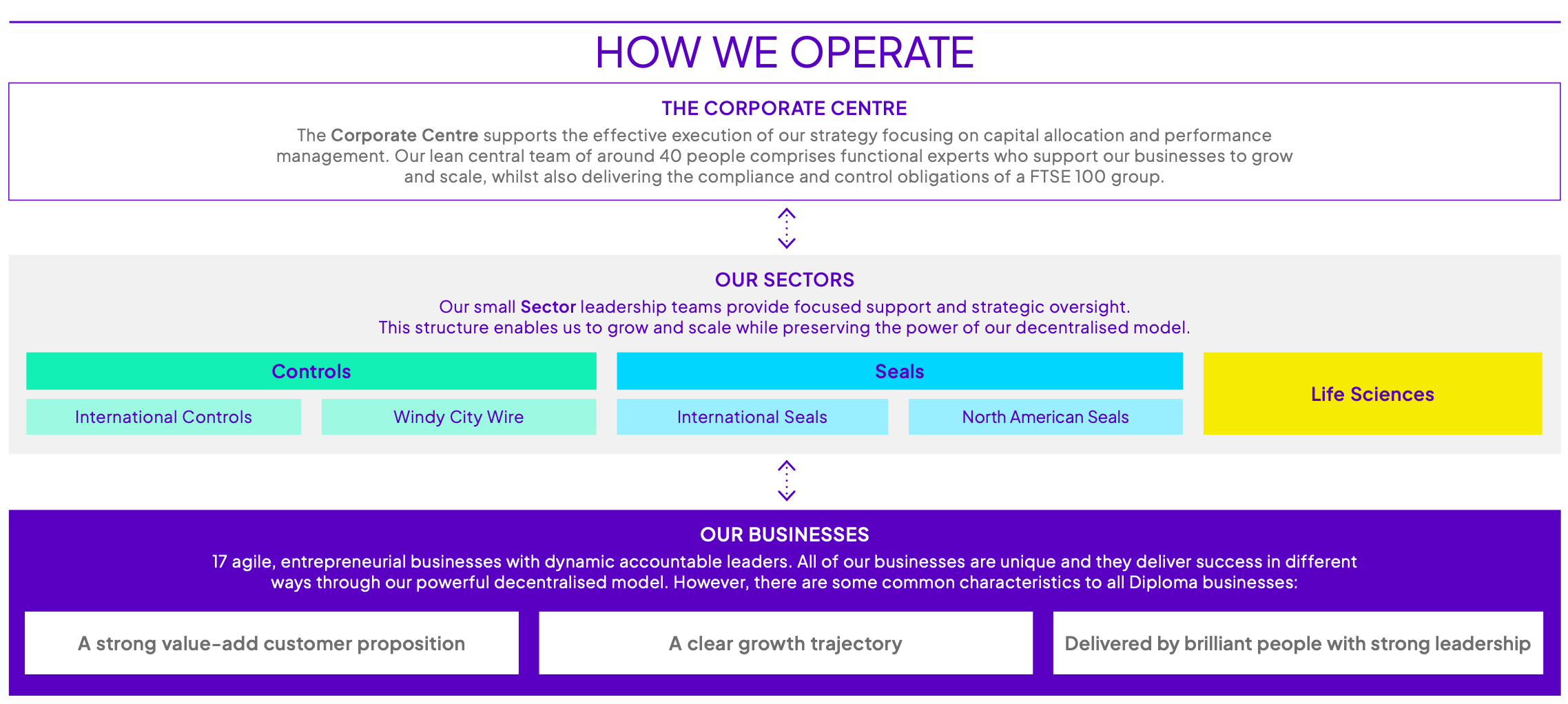

When thinking about Diploma, their strategic shift toward focusing more on organic growth and end market exposure they know well resonates closely with HEICO’s operating model.

We have a decentralised approach, which means that we have really fantastic, brilliant local management teams, they’re very accountable people, very commercial, humble, and focused on continuous improvements, and they’re therefore very good at execution. And it makes them dynamic, it makes them agile, and therefore they tend to do very well in volatile times as a result of that. And we saw that, I mean, I saw that clearly through the pandemic. - CEO Johnny Thomson (May 2025)

This report will cover:

Part I - Executive Summary: Why Now? What’s made us cover (and own) Diploma?

Part II - Diploma’s Business Model

Part III – Diploma 2.0 – More Ambition but Loyal to the Model

Part IV - M&A Philosophy, and Thoughts on Decentralization

Part V - Large M&A & Recent Developments

Part VI - Base Case Valuation and Input

Part VII - Conclusions

Part I - Executive Summary: Why Now?

A. Growing Up

In the past, those of you who’re already familiar with Diploma heard Johnny Thomson, the CEO, talk about “growing up” and that's visible in many aspects. Thanks to the increased size, financing M&A and digesting larger deals has become easier and whenever Diploma seeks to acquire a substantial asset, it does not have to raise capital anymore - as it did for the Windy City Wire, T.I.E., and DICSA transactions. It’s also become more transparent about its M&A disclosures.

Another element is that Diploma’s now got an executive leadership team working together with the CEO, while the individual subsidiaries’ operations are fully decentralized. Because of this, this serial acquirer blends top management accountability and acquisitive capital allocation, and decentralization to develop each business’ organic growth.

Our customers, our value propositions, our management, performance, strategy, they're all local. Success happens for us at the front end and that also defines how we behave too. - Johnny Thomson

Looking at Diploma today versus the pre-Thomson era, the core foundations haven’t changed much, though. The principles around value-add remain but there’s now a loud-and-clear ambition for delivering stronger organic growth. In his opening remarks during the 2026 Redeye serial acquirer conference, Diploma’s CEO stated:

We might be a slight imposter in the room. We’re not a serial acquirer.

The reasoning behind this seemingly controversial statement (Diploma is a serial acquirer, of course) is that the focus on organic growth is the number one priority.

In his mind, acquisitions should unlock future organic growth potential. Or put another way, M&A will dictate how successful Diploma’s organic growth and future compounding journey will be. Furthermore (and this isn’t given much thought by investors), if you’re deploying capital into poor IRR acquisitions, you’ll dilute the success of previous and ongoing successes.

B. The Investment Thesis For Diploma In 2026 and Beyond

The PDF of this write-up can be downloaded below.