Lifco AB

The best industrial serial acquirer?

Lifco AB is one of the leading Swedish serial acquirers that focuses on acquiring, managing and developing market-leading niche businesses. "A safe haven for your business", aka perpetual ownership and steady compounding.

Exhibit I (Lifco investor presentation)

Lifco traces its history back to 1946, when the Swedish county councils established a central purchasing entity for medical equipment and services. During the 1990s, Lifco underwent several changes in ownership and name. In 1993, it was acquired by its management team and the venture capital firm Procuritas, and was renamed Lifco AB, becoming the parent company of the current Lifco Group. From 1995 to 1998, Lifco operated as a division of the public company Getinge Group.

Following a strategic shift by Getinge, Lifco's ownership was distributed to Getinge's shareholders in 1998. In 2000, Carl Bennet AB determined that Lifco needed restructuring and would perform better as a private company. Consequently, Lifco became a wholly-owned subsidiary of Carl Bennet AB.

In 2001, Lifco shifted its focus to the distribution of dental products, leading to the divestiture of its health and self-care operations, which accounted for 40% of its total sales.

In 2006, Lifco then went ahead with the acquisition of its sister company Sorb Industri AB, a diversified industrial company also owned by Carl Bennet AB. A new industrial serial acquirer was born. This somewhat resembles Warren Buffett's Berkshire Hathaway, which started as a textile manufacturer and eventually transformed into a massive conglomerate.

Over the past few years, we've learned a great deal from Lifco’s current CEO Per Waldemarson and former CEO Fredrik Karlsson (who became the co-founder and CEO of Röko, a newly created sector agnostic serial acquirer). Together with Mark Leonard, they’ve shaped our public investment strategy and previous professional M&A practices: focus on profitability, excellent cash performance, high ROIC/ROIIC, reinvestment rates, and proactive use of a healthy balance sheet. To us, true profitability and cash flow is key to a company’s longevity.

Earlier this year, Karlsson stated:

The nice thing having a high profit margin is: it’s easier to have a nice cash flow and when there’s a problem at one of the companies, you don’t have to inject new capital.

Turning back to Lifco. It now operates across three business areas: Dental, Demolition & Tools, and Systems Solutions, all covering an extensive geographic reach. Over time, the entire Lifco group has entered new markets and diversified away from Sweden, as shown in exhibit II.

Exhibit II (The Compounding Tortoise)

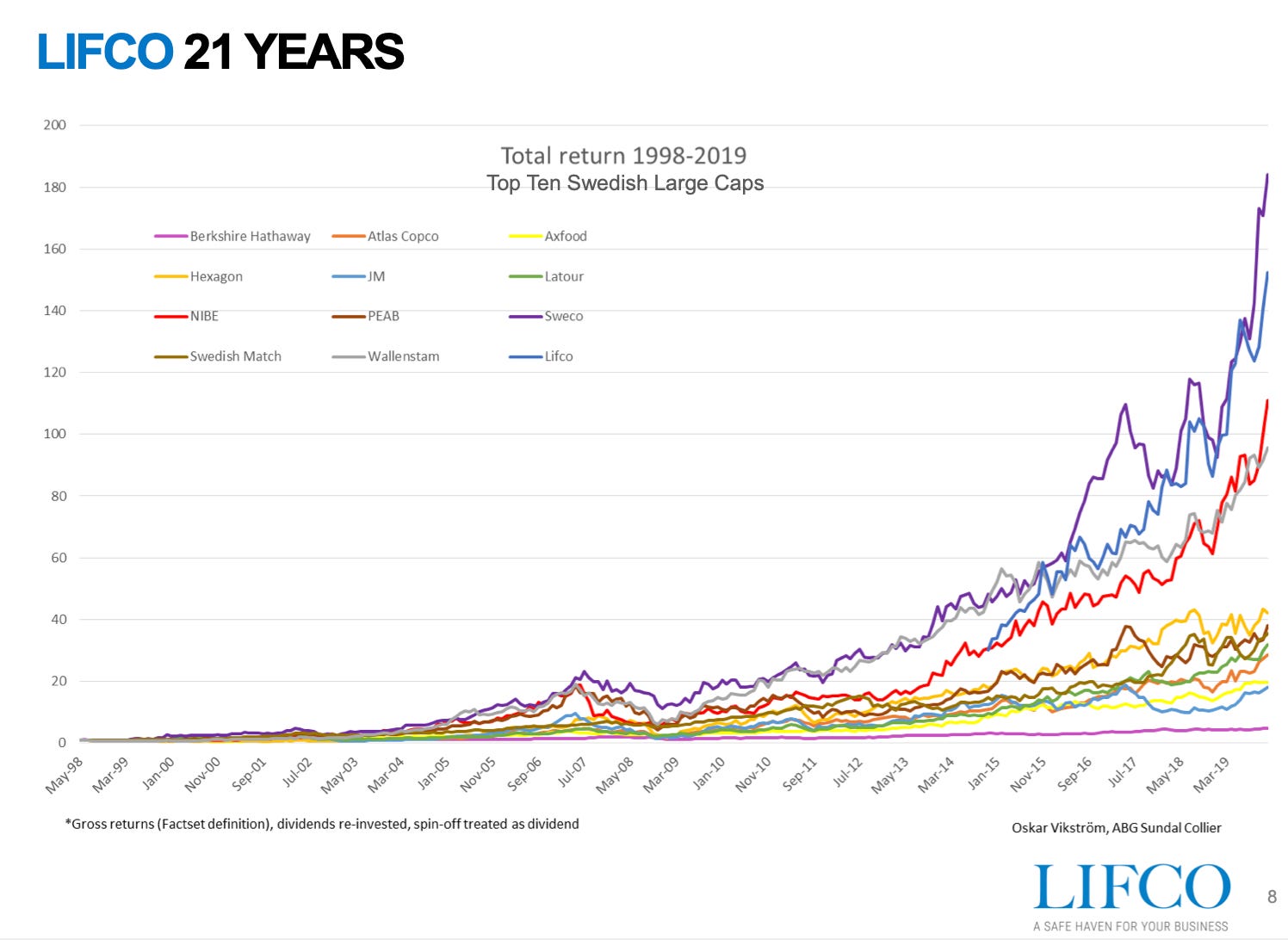

Exhibit III highlights Lifco's total shareholder return from 1998 to 2019, providing context around its long-term track record following its first five years as a listed company. Since 2019, Lifco's stock has increased by an additional 176%, excluding dividends.

Exhibit III (Lifco Q4 2019 report)

So, how’s that possible? Strong profit and cash performance, and redeploying cash back into M&A (to put it simply). Since 2006, Lifco has completed or announced 131 acquisitions, or about 8 annually.

Coupled with organic growth and operating leverage, total EBITA (excl. acquisition costs) has compounded by 18.3% per annum as per the last twelves months (Q2 2024 data). Exhibit IV depicts EBITA and the year-over-year delta.

Exhibit IV (The Compounding Tortoise)

Lifco has one clear objective: to improve profits every year (and organically in every subsidiary). It has so far only failed twice, with 2013 showing a negligible decline, also because there were no new acquisitions. The recession of 2008-2009 hurt the more cyclical subsidiaries in Demolition & Tools, but fortunately there was still the steady as she goes Dental business. More on the segment performance later. Exhibit V highlights Lifco’s organic EBITA growth at incrementally better margins.