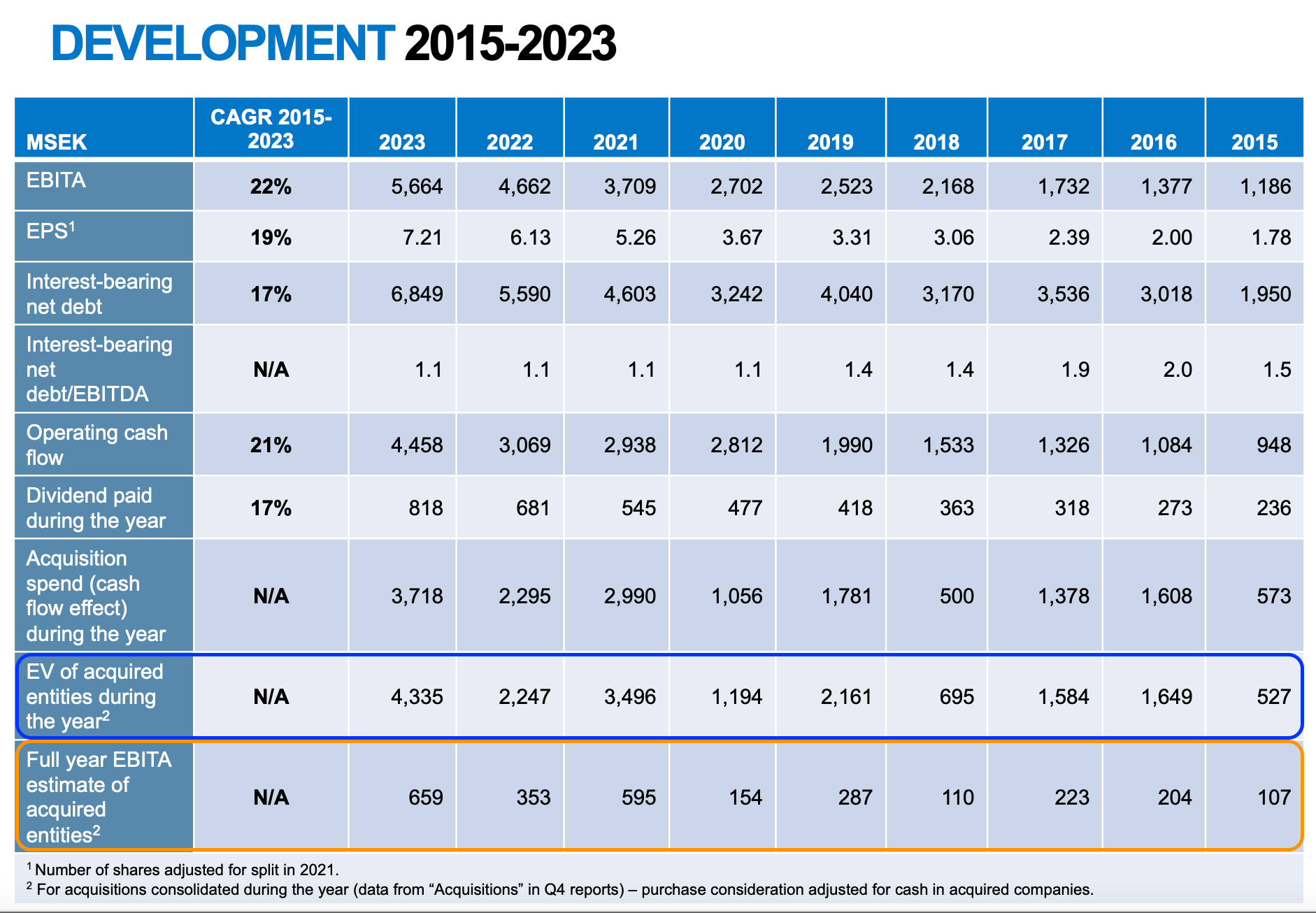

How Can Lifco Continue to Acquire at Such Low Multiples?

How Can Lifco Continue to Acquire at Such Low Multiples?

Profitability dispersion: recent past versus present

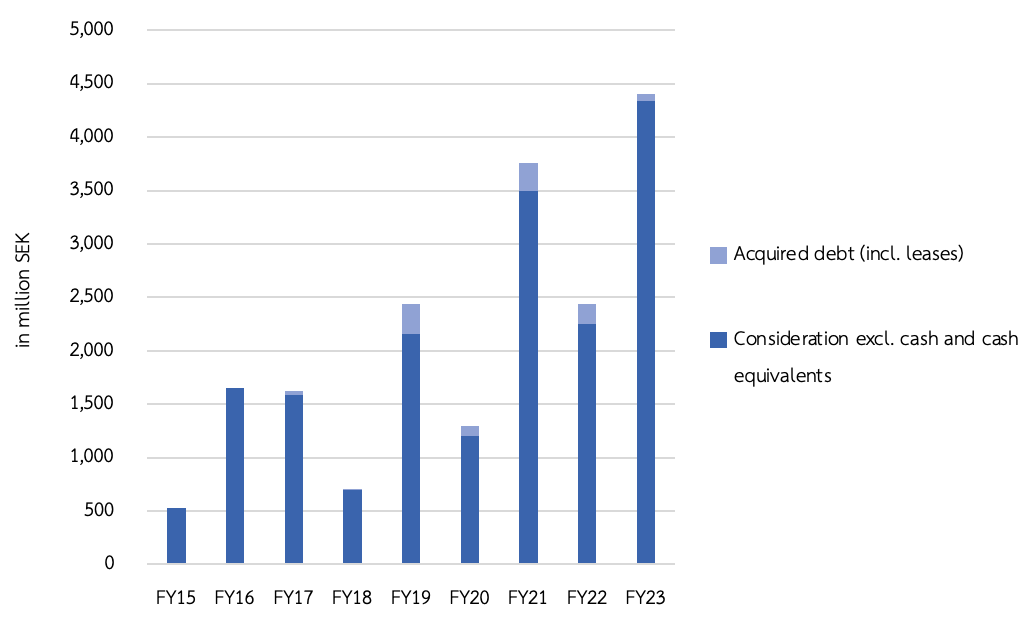

Last week, the Lifco earnings call Q&A was somewhat dominated by questions around the low multiples paid for acquisitions. Analysts referred to this below slide.

Consideration Paid vs. Total Enterprise Value

The reported enterprise value is the aggregate consideration paid (or to be paid in the future when Lifco buys the minority shareholders’ stake, the put-call debt related to the minority shareholders is then constantly being revalued based on the subsidiary’s performance) excl. cash.

Additionally, we must add the borrowings and lease liabilities of the acquired entities (at the time of consolidation) to this equation (which didn’t happen in the above slide). There’s no watertight figure on the lease liabilities related to the scope of consolidation. Instead, we used the change in right-of-use assets related to acquired companies as a proxy. For FY23, we’ve penciled in some 70M SEK in acquired debt. Still, it’s pretty immaterial to the multiple paid (it would be more relevant if Lifco were to acquire retail chains).

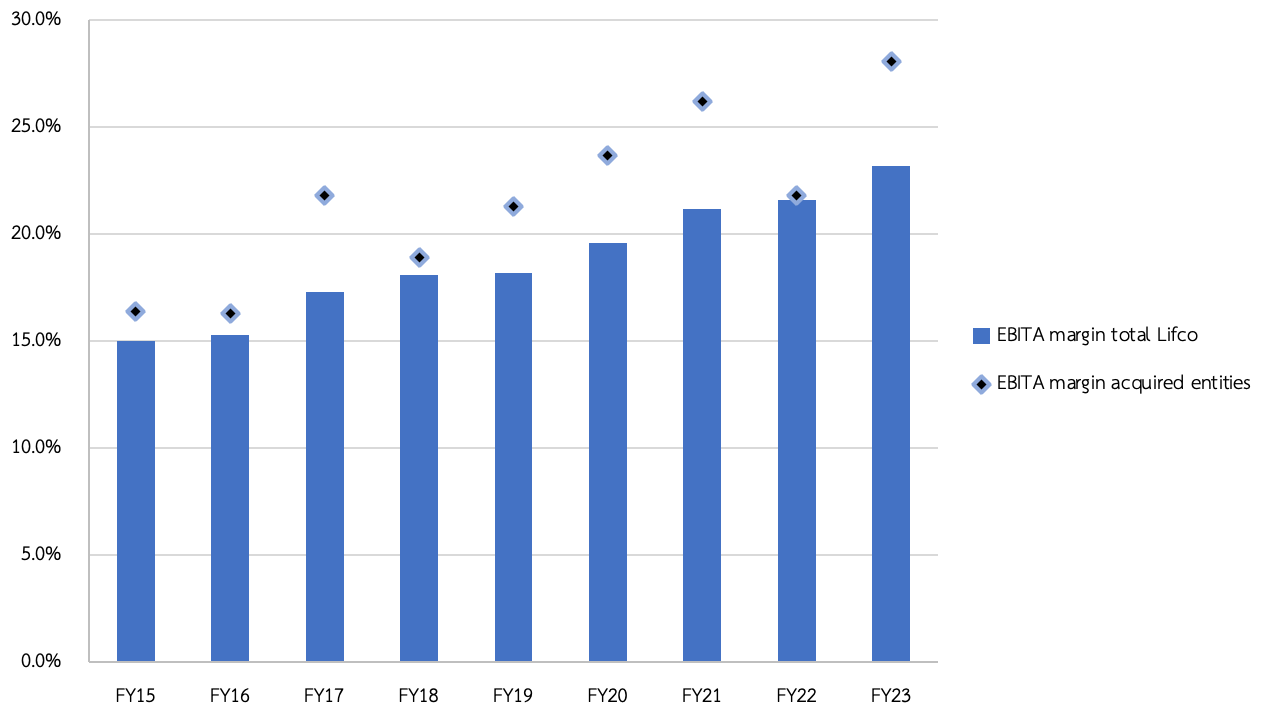

Acquired Annualized EBITA

The acquired annualized run-rate EBITA is management’s estimate of the total annual contribution in the year of consolidation; it’s not a watertight calculation as it could depend on business seasonality, special orders et cetera. Also, the Lifco family consists of more defensive businesses (Dental) and more cyclical ones (Demolition & Tools).

Lifco gives us the aggregate EBITA contribution for all executed M&A transactions. Considering the timing of acquisitions (and the contribution from previous year’s acquisitions that hadn’t yet entered the organic comp base) figuring out mix effects from M&A on the total Lifco EBITA margin in any given year cannot be done accurately.

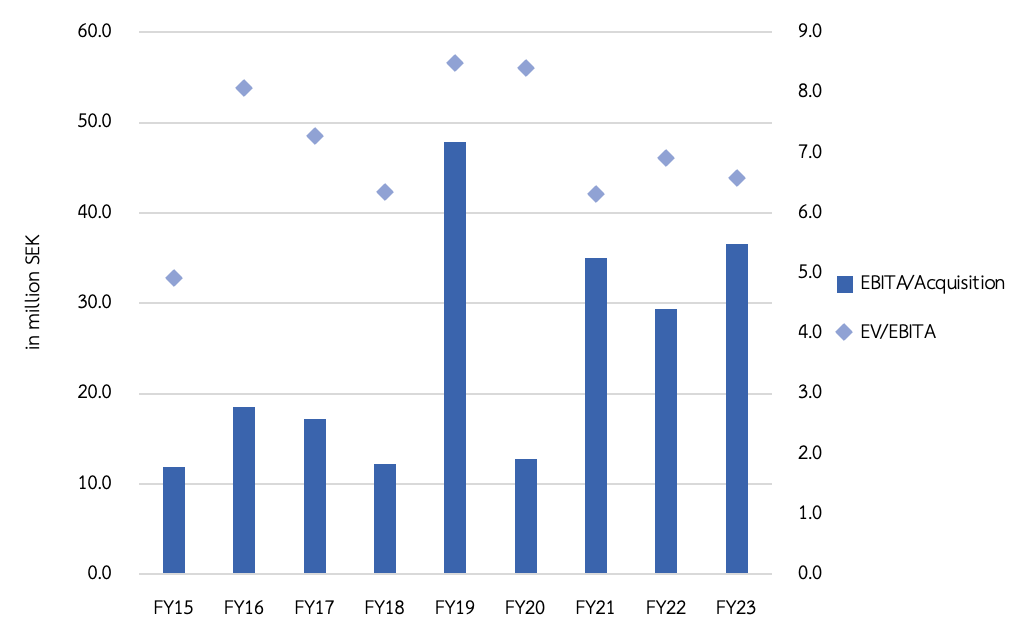

Hypothesis on Why Lifco’s Multiples Paid are Low

We believe Lifco's M&A strategy is greatly outperforming other industrial serial acquirers’ and the reported EBITA multiple reflects a considerable margin of safety. Here’s just a food for thought hypothesis: we don’t have the exact data to back this up, but it’s based on common sense and what we’ve seen in our professional M&A portfolio.

The low reported multiples and thus elevated IRR right from the start versus other serial acquirers such as Indutrade can only be explained by a wide profitability dispersion: recent past/three-year average versus present. When Lifco closes a deal, they must have taken multiple years into consideration. It would be foolish to be buying at what could potentially be peak margins. Now of course, which year's profit metric will they report to investors? Not the EBITA figure from the past (e.g. 2020 or 2021) but today's profitability.

Deduce from that: Lifco bought many excellent companies that had already started to enjoy margin expansion, long before Lifco's best practices drove profitability to even higher levels.

Consider the following example to illustrate our thinking.

EBITA in 2020: 10 million SEK

EBITA in 2021: 13 million SEK

EBITA in 2022: 14 million SEK.

Run-rate EBITA when Lifco took over in 2023: 16 million SEK.

2020-2022 average: 12.3 million SEK.

9x (i.e. a realistic multiple) the average EBITA gets you to 98 million SEK. Compared to the current run-rate: 6.3x. And that’s the multiple analysts arrive at, based upon the reported LTM figures.

We’ve witnessed a growing EBITA profitability lag for some of our M&A cases as well. A company with an average EBITA margin of 18% that finally managed to pass along price increases to its customers saw its profitability grow to 25-30% (in just 1.5 years). Understandably, the multiple paid for the acquisition was based on the two-year average marginality prior to closing the deal, as private SME M&A is based primarily on backward-looking/already known profitability and revenues.

The magic of having underpaid for a business (always in hindsight) is only valid to the extent that the companies acquired do have durable pricing power and operate within an attractive, fragmented niche (with below-average cyclicality). In other words, the profitability step-up should not be considered a one-off event.

We argue that margin expansion and cost-pass-through inflation in Lifco's subsidiaries are the most important factors in explaining the low reported multiples paid for recent acquisitions that we're seeing today.

Prior to 2020, Lifco tended to pay up for better profitability/quality businesses as margin expansion growth prior the Lifco acquisition must have been smaller. So, the difference between the three-year average EBITA and the EBITA at the time of acquisition was likely smaller that time.

Lifco's M&A strategy has so far been accretive to overall profit margins. The companies they're buying have even stronger profitability than the existing Lifco family.

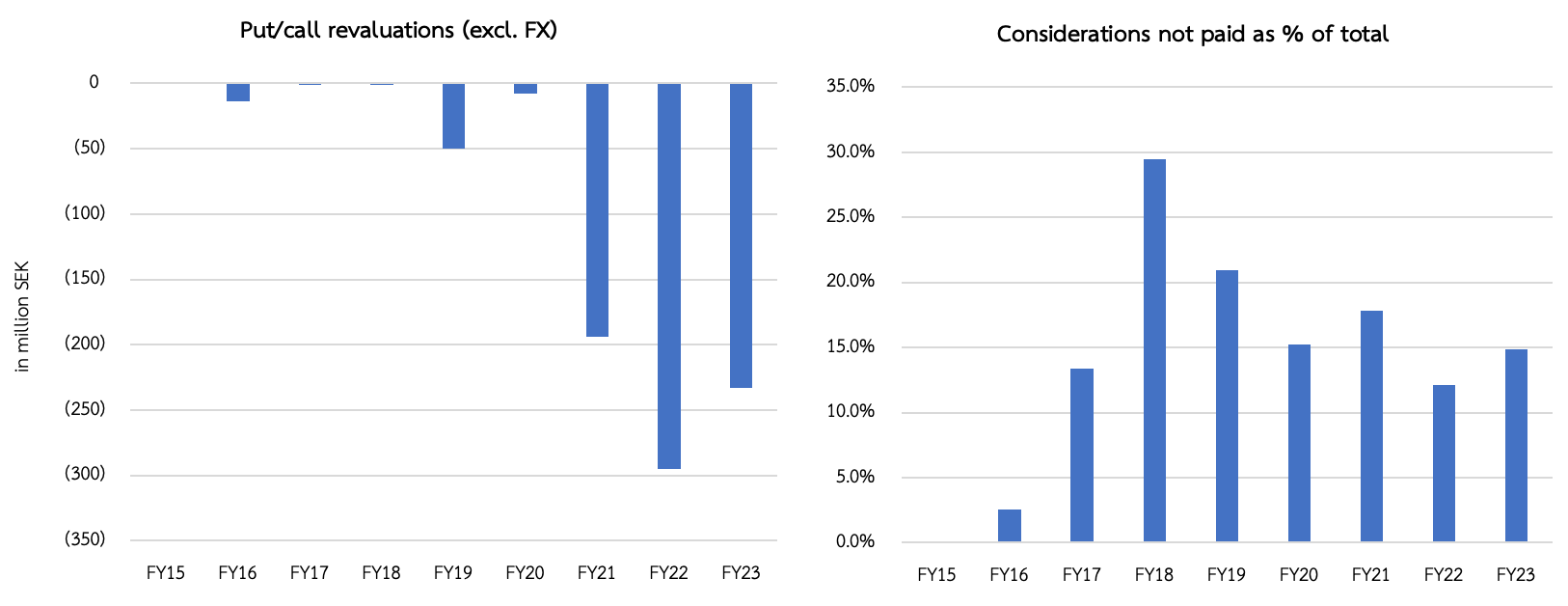

Put-Call Debt Revaluations

Another way of looking at the strong M&A execution relative to management's initial expectations: the sizable revaluations in mandatory put-call debt related to the minority share shareholders. Again, as an outsider, it’s quite difficult to know the puts and takes from the put/call debt fair value and the subsequent revaluations.

By 2026 and solely based on normalizing margin expansion (<50 bps per annum), we expect Lifco's multiples paid for acquisitions to gradually normalize towards 8-9x EBITA. If Lifco can continue to do these low-multiple acquisitions, then Per Waldemarson and co have the touch of Midas.

Interested in learning more about serial acquirers, the Lifco earnings report and/or our portfolio strategy? Then subscribe via the below button!

Like LifeCo there are a few other companies that are considered compounders by some in Sweden (like TEQ maybe). Sweden has a macro policy to use a weakening currency for their advantage. As a US resident, if I buy Swedish based businesses, the erosion of SEK to USD is quiet painful on returns. Since 2021 almost 20% for example. Do you hedge that or is there someway to think about that when allocating?