How to Define NOPAT - Constellation Software and Linde Plc

How to Define NOPAT - Constellation Software and Linde Plc

Valuation should be based on common-sense with no accounting gimmicks

In this article, we’re going to provide additional colour on one of our previous posts: how to value companies. It’s still more art than exact science.

Given that we’re focused on quality growth companies, the terminal value will play a key role in assessing long-term upside potential and thus the implied IRR.

We look at terminal value from a NOPAT perspective rather than reported FCF which is oftentimes distorted by:

differences between growth and maintenance CAPEX (with NOPAT, we try to get a sense of the recurring capital intensity);

amortization of acquisition-related intangibles (very relevant for serial acquirers to juicing the post-acquisition returns);

potential changes in investment policy: leases versus CAPEX

To us, both FCF and NOPAT should include share based compensation. They are treated as any other operating cash expense.

While SBC theoretically is a non-cash expense, you’d either have to buy back shares to offset dilution (which will affect the net financial position) or model for persistently growing dilutive effects (difficult exercise).

NOPAT is a common-sense based metric and represents our one and only proxy for steady-state free cash flow (it adjusts for the above described discrepancies in FCF, regardless of how a company is being financed, just the same way as we would approach ROI(I)C).

NOPAT to common shareholders could be calculated as follows: total consolidated EBITA x (100% - T) adjusted for non-controlling interests.

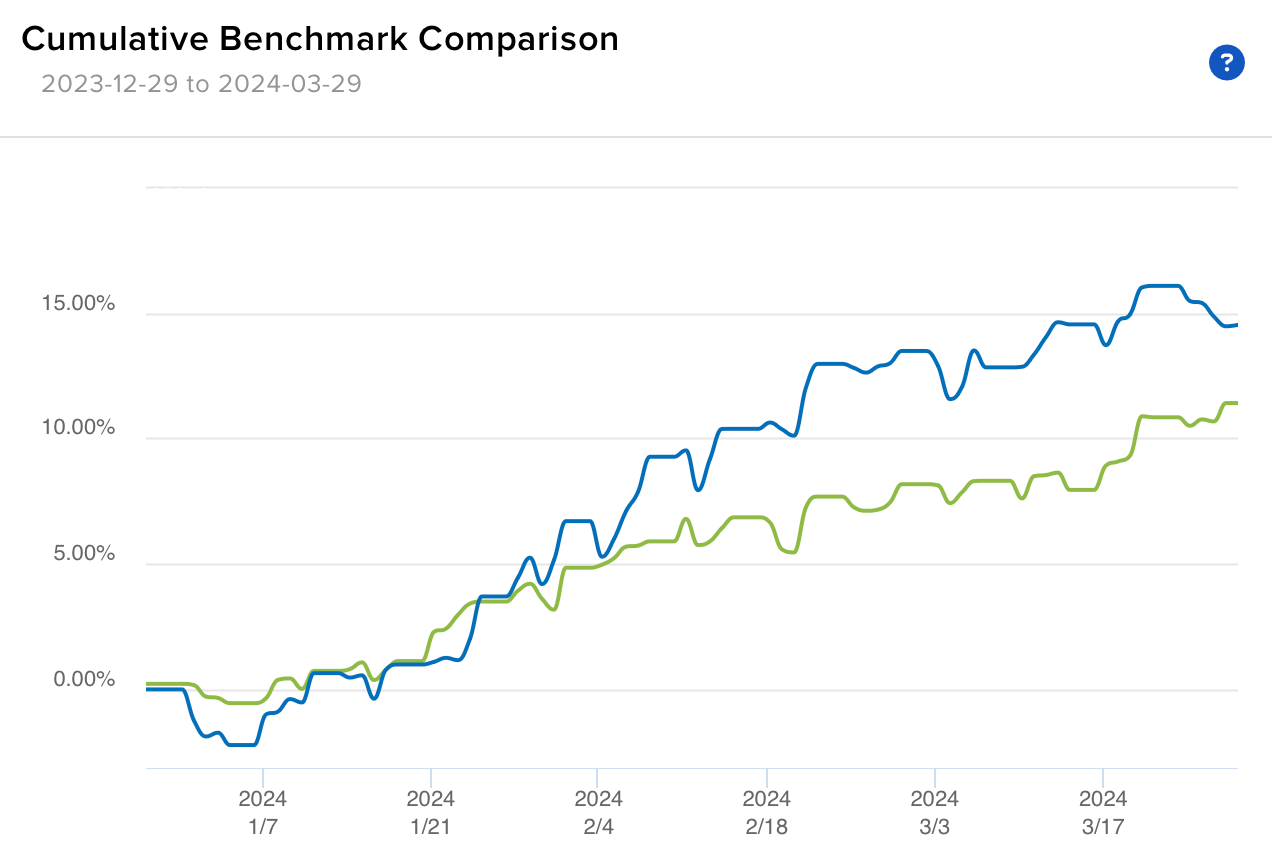

Q1 Performance

Before we get into the details, let’s first take a look at our Q1 performance. We finished the first three months of 2024 with a +14.55% return (vs. the index' 11.42%).

As you know, we’re interested in one thing only: achieving our absolute return goal, as comparing your performance too often to the indices’ will make you very short-term focused. Still, a 14.55% (fully-invested) return over a short time period isn’t really what we would call a Tortoise result. But frankly, we don't care about the short-term performance and Q1 has been very good to many investors. So should we consider Q1 to be a lucky shot: time will tell.

It will be interesting to watch our performance during periods of heightened volatility, resurgent inflation and thus uncertainty. We target positive alpha primarily during down markets, which forces us to think deeply about a selective group of outstanding compounders. Compounding starts with protecting the principal.

Aside from the short-term narrative around stock market performance, we focus on the underlying NOPAT per share evolution (incl. share buybacks) and our companies' left-over cash flow being distributed back to shareholders.

Enjoying a 14.55% return simply means short-term valuation multiples have re-rated but that shouldn't pose a threat to generating strong IRRs on new purchases going forward. That's what we're going to make crystal clear in our first "Letter to Our Partners" set to be published on the Substack mid-April. Keep your eye on the fundamentals, not the speculative nature of the stock market.

We hold boring businesses that have crushed the market over the past 3, 5, 10 and 10+ years. Making money with old friends, as Terry Smith once said.

Constellation’s Acquisition Strategy and Amortizations

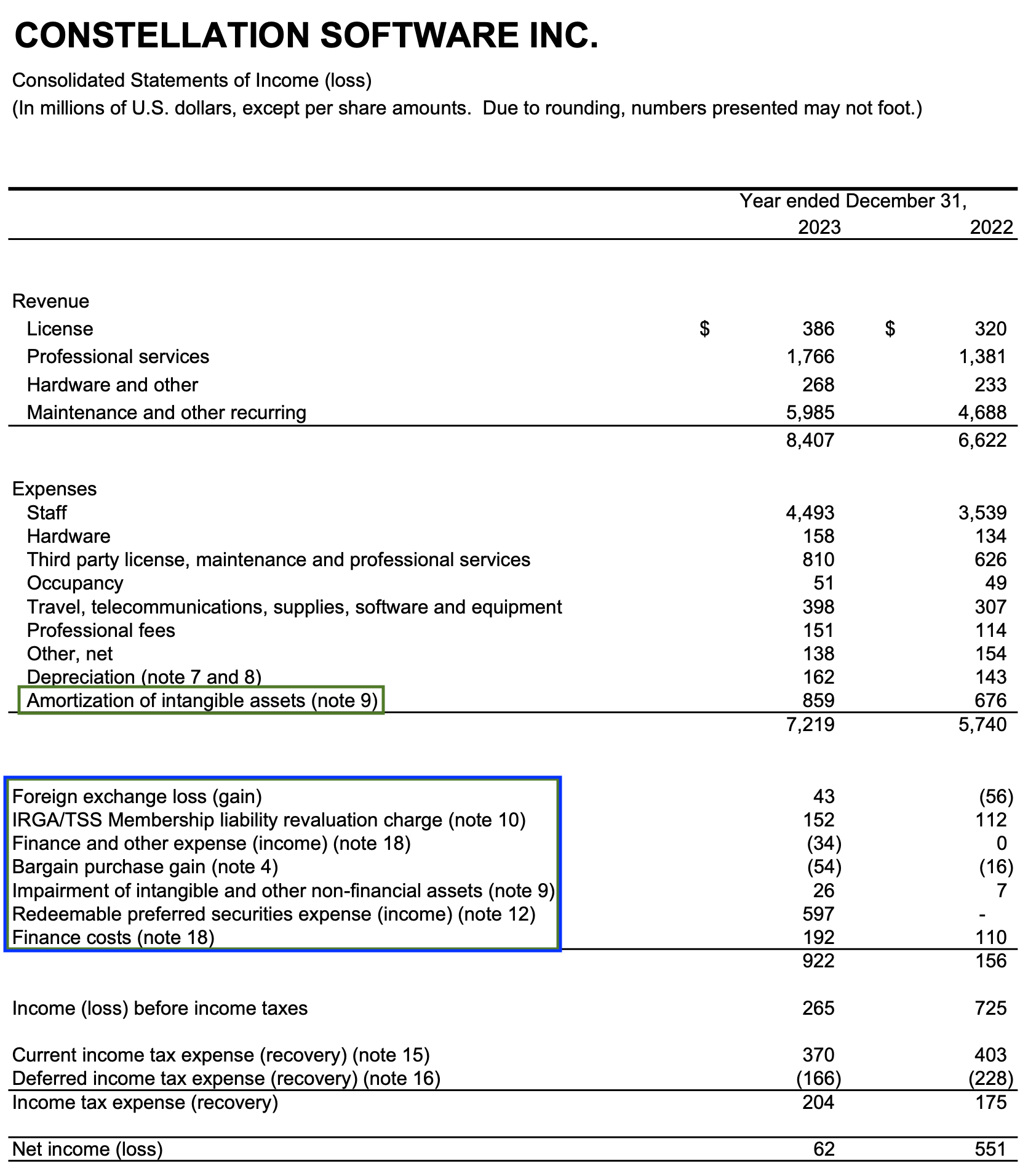

Kicking off the NOPAT discussion, Constellation Software’s financials look pretty complex from the outside. Ignoring the existence of non-controlling interest for just a moment, reported net income is nowhere near the underlying NOPAT and free cash flow figures.

How should we calculate CSI’s NOPAT?

Income before income tax = 265 million USD

+ all other expenses and - all other income (highlighted in blue) = 922 million USD

+ amortization of intangible assets, only to the extent that these are purely acquisition-related (859 million USD).

Amortization of internally capitalized costs shouldn’t be added back to EBITA as they are part of a company’s organic growth strategy. They are in fact equal to depreciation.

Moreover, the effects from capitalizing costs on NOPAT and free cash flow assumptions require careful analysis (e.g. Vitec). For Constellation Software, R&D is being expensed and not capitalized, making things a lot easier.

This is now the fully-consolidated EBITA (2.046 billion USD) from which we then have to deduct normalized tax expenses to get to NOPAT, before adjusting for NOPAT belonging to non-controlling interests.

The main difference between FCF (ignoring the interest charges) and NOPAT: as long as Constellation Software continues to pursue its M&A strategy, it will benefit from the above amortizations to lower the tax burden. As such, our IRR model will have to take these benefits into account.

However, under a steady-state scenario, we’ll assume CSI cease doing acquisitions which will ultimately cause the amortizations to disappear after 8-9 years (and thus no additional tax savings). One could still estimate the residual value of tax reductions from amortizations for acquisitions that are likely to be concluded 8-9 years prior to reaching the steady-state NOPAT. To be fair, this adjustment won’t move the needle that much.

Linde Plc and the Merger Effects

In 2018, Praxair and Linde AG completed the merger. And while some investors doubted its merits, Linde Plc is now the world’s leading industrial gases and engineering company with top-notch operating margins and return on capital, the latter often referred to as being the “truth serum” for its capital allocation strategy. Unsurprisingly, non-cash purchase price accounting impacts caused its reported to profits to deviate heavily from underlying NOPAT and FCF.

For years, we’ve been told: look at Linde’s high P/E ratio (40+). Not contextualizing its seemingly elevated P/E ratio and consequently not buying its shares would have led to you miss out on a 170+ % total return over the past five years. The high P/E doesn’t make any sense given the specific circumstances created by the merger… You should never take a reported income number at face value. On the other hand, the non-GAAP adjustments performed by the management team should be gauged carefully. Do these adjustments reflect underlying performance (i.e. are one-offs really exceptional)?