LVMH - FY 2023 Earnings Discussion

Re-accelerating growth in Q4 & bullish on 2024

The results from the luxury juggernaut have been awaited eagerly and here they are: re-accelerating growth in Q4, with a strong performance in US and Asia (excl. Japan) and a positive take on 2024. Let’s guide you through the main takeaways and what the LVMH results imply for our luxury tilt (to which we’ve added recently) and which names we deem the most attractive.

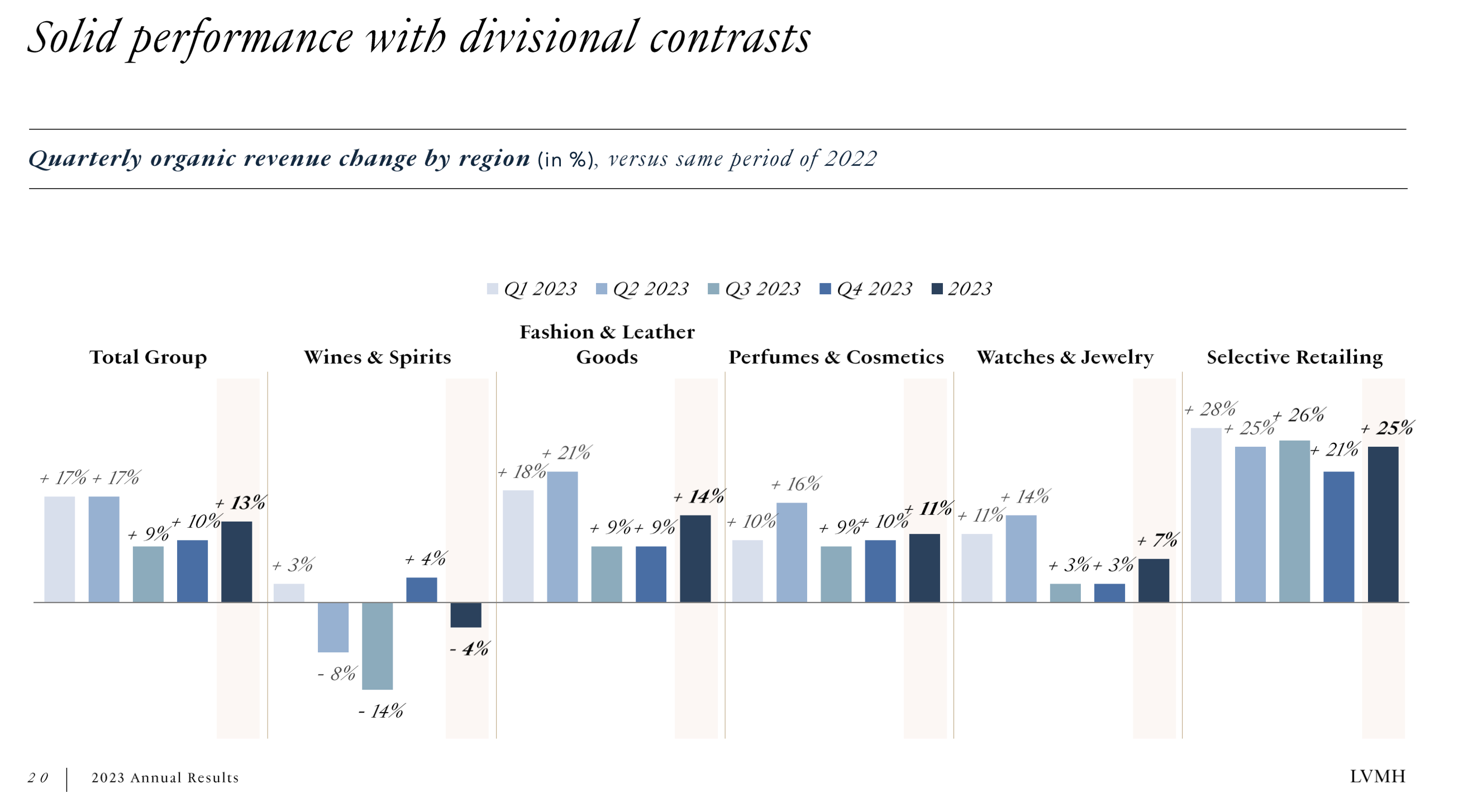

“Wines & Spirits” - Really the Only Segment Distorting the 2023 Growth Trend

All in all, we believe LVMH’s Q4 results confirm the attractiveness of the Maison during challenging economic times. Its CEO Bernard Arnault stressed the importance of creating exclusivity and refraining from achieving “too much” growth. Quiet luxury they call it.

We’ve highlighted the challenging comps that luxury companies faced during 2023 in our previous podcast. And even within this well-defined consumer discretionary sector there were some widely differing performances last year. Burberry’s execution remained weak (it’s like a turnaround that simply doesn’t and maybe won’t turn), whilst Hermès continued to exploit its unmatched status of exclusivity and quality.

Turning back to LVMH. Looking at the sequential performance, it posted accelerating growth in both the US and Asia; the former saw a rather weak Q2 and Q3. Growth in the core business (“Fashion & Leather Goods”) was overshadowed by the shrinking “Wines & Sprits” (which accounted for approximately 10% of total 2023 EBIT). When every segment is performing pretty well - despite recessionary talking - except for one, then investor perception won’t work in your favor. Especially during times when the luxury sector has already witnessed many distortions in the underlying growth trend.

However, such behavior typically creates buying opportunities for those who see through these temporary headwinds. The COVID-19 reopenings led to an uneven recovery in developed versus emerging markets, which was followed by higher interest rates, inflation, the war in Ukraine et al. More than others, luxury companies got punished by elevated volatility (both upwards and downwards), which caused some investors to go into a wait-and-see mode till the dust (finally) settled. And we’ve probably reached that point of stabilizing comps in Q4 2023.

All in all, we judge LVMH’s Q4 outperformance to be largely driven by a rebound in “Wines & Spirits” as the core businesses have held up pretty well throughout 2023. In our opinion, there was little to be worried about in the first place. For Asia, we should be cognizant of the easy comps in 2022. Still, seeing a quarter-over-quarter pickup in total revenue growth should help investor sentiment improve.

Margins and Cash Flows

LVMH’s total top line growth was comprised of 13% organic growth and a 4% FX translation headwind. That 9% growth trickled down to the entire P&L with virtually no operating leverage (G&A expenses rose 14%). In fact, EBIT growth was a tad lower at 8%, contrasting with Hermès’ situation (its EBIT margins are supposed to have grown by 80 bp over the past year).

In terms of cash flow, growing sales and inflation led to a substantial increase in working capital. Cash from operations after taxes paid (including lease D&A which is then offset by a similar cash outflow related to the lease repayments) amounted to 23.8 billion EUR.

After adjusting for lease D&A and financial costs, total cash available for growth investments (CAPEX, working capital and M&A) came in at 20.2 billion EUR. LVMH was pretty aggressive in terms of investments as total CAPEX were 7.5 billion EUR.

On top of that, the underlying growth in ROU assets excl. FX (this change won’t show up in the investing cash flow, aside from leasehold improvements) stood at 1.5 billion EUR. All things considered, LVMH’s free cash flow shrunk to 8.1 billion EUR, slightly exceeding the dividend payment (but little concerning).

Without a doubt, LVMH is prepared for future growth, so let’s try to examine the yearly return on those investments. Given the nature of LVMH’s business (durable and oftentimes one-time large investments in stores, buildings) reported ROIC may be overstated. After all, ROIC is based on the book value of invested capital. Ideally, we should correct for inflationary impacts as we’re interested in the return potential for future investments.