One of the Best Terry Smith Interviews to Date - 6 Highlights

How to use compound interest to grow your investments

We oftentimes re-read books/blogs/papers or re-listen to interviews/podcasts to remind ourselves of what is we’re trying to do: focusing on a select group of excellent companies and understanding what has made, makes, and hopefully will continue to make them special and highly rewarding for long-term shareholders.

Recently, we’ve broken down the principles of McKinsey’s Valuation Book, and unsurprisingly, it’s already one of our most-read blogs ever.

Today, we’re highlighting one of Terry Smith’s 2024 interviews. Known for his usual insights into Fundsmith’s performance and portfolio holdings - delivered with his British humor - he talked about other basic ingredients on how to compound your capital.

In this blog, we’ll share our own perspective on his analysis process and relate it back to our portfolio strategy and companies.

1️⃣ Compounding: Letting Our Companies Reinvest for Us

Smith’s opening remarks during this interview were as follows:

One of the least talked about characteristics of equities, stocks, stock market and investment is it's the only asset class which can compound. Others can't do it. Bonds can't do it. If you own bonds, even if everything goes well, they just pay you interest. And then when they get to their maturity, they pay you back. They don't reinvest any of your cash flow from the bonds.

Property is the same. If we own this building that we are here in today, presumably we would get paid rent. And at the end of the lease, we could either renew the lease or sell the building.

But none of the money we receive would be reinvested in property for us. Whereas in equities, some, around about half, approximately, of companies' profits are retained and reinvested in the business. And if they do that tolerably well, it compounds in value.

We’ve talked about return on invested capital, return on incremental invested capital, cash IRRs, opportunity costs… before. Our latest series on “Sustainable Quality Compounding” covers these aspects in great detail.

One of the points of criticism - brought up by many as Fundsmith’s underperformance has grown - around Smith’s strategy is that he’s too focused on on past winners. The Fund’s return on capital employed figure is a lot better than the index, but we’re not interested in the rolling returns: we’re buying future successes, and adjusted for inflation (which has had a favorable impact on companies with long-lived assets).

If you're thinking of investing in anything else, a bond, my fund, you want to know what do you think the return will be? Why don't we ask that with companies? We should. - Terry Smith

Anyway, this first key point is critical: we seek compounders. We need growth, solid returns on newly invested capital, and a healthy reinvestment rate to harvest the beauty of equities: compound interest. In every quarterly letter, we clearly state the necessity for every large holding in our portfolio to keep delivering on the 10-plus percent CAGR in NOPAT per share, underpinned by high returns on incremental invested capital and proactive excess cash management.

2️⃣ Diversification vs. Focus

There aren’t that many companies that should make it to our investable universe, and eventually, our portfolio. Sufficient diversification (like the best-of-breed names in Vertical Market Software, High-End Luxury, Industrials…) allows us to stay focused on what matters most: letting companies compound our capital at high rates of return, because they’re run by excellent people (culture determines).

People rarely study what he (Markowitz, Nobel Prize winner for his efficient frontier) actually said and its limits. He didn't say that diversification has an infinite and linear contribution to investment. Once you get beyond a certain number of holdings, you've achieved all the diversification benefit you're ever likely to achieve. - Terry Smith

At the end of the interview, Smith also talked about coming up with new ideas.

So that's the biggest one, is the desire for new ideas, right? And it's partly driven by people thinking that they've got to make their contribution not through doing the day job, assiduously working through the numbers in the accounts, making sure the database is there and so on, but thinking, oh, well, if I come up with this new idea and it sort of blows the door off, the boss will be terribly pleased. And that's, I think, the biggest bias amongst people.

It’s one we struggle with too. We’re running this Substack newsletter, and people frequently ask us about what stock we’ll cover next or add to the portfolio. What’s on your watchlist? Obviously, you’re paying for a monthly or annual subscription, so there’s a natural desire for learning about new companies.

Interestingly, we’ve rather taken the opposite view and decided to debunk the real drivers of shareholder value creation by concisely highlighting excellent and not so excellent companies with structural advantages or challenges. Frankly, we don’t feel there’s much value-add in describing tens of quality companies very vaguely, looking at backward-looking metrics; or simply: being master of the obvious. This approach is also reflected in our concentrated portfolio strategy.

3️⃣ Defining What You Want to Own, But Don’t Label Too Much Imho

Labeling isn’t all that helpful, but sifting through general industry definitions and the related returns on capital helps narrow down the investable universe.

We won't invest in banks, insurance companies, or real estate businesses. We won't invest in companies involved in minerals, mining, exploration, oil, gas, et cetera, et cetera. We won't invest in utilities. We won't invest in airlines and logistics businesses. There's a few examples for you. There's quite a few. - Terry Smith

Sometimes, you’ll find a compelling name in an industry that’s filled with un-investable options. We ended up owning O’Reilly and AutoZone, and they’ve been incredible solid performers for us, even though the average retailer has done quite poorly.

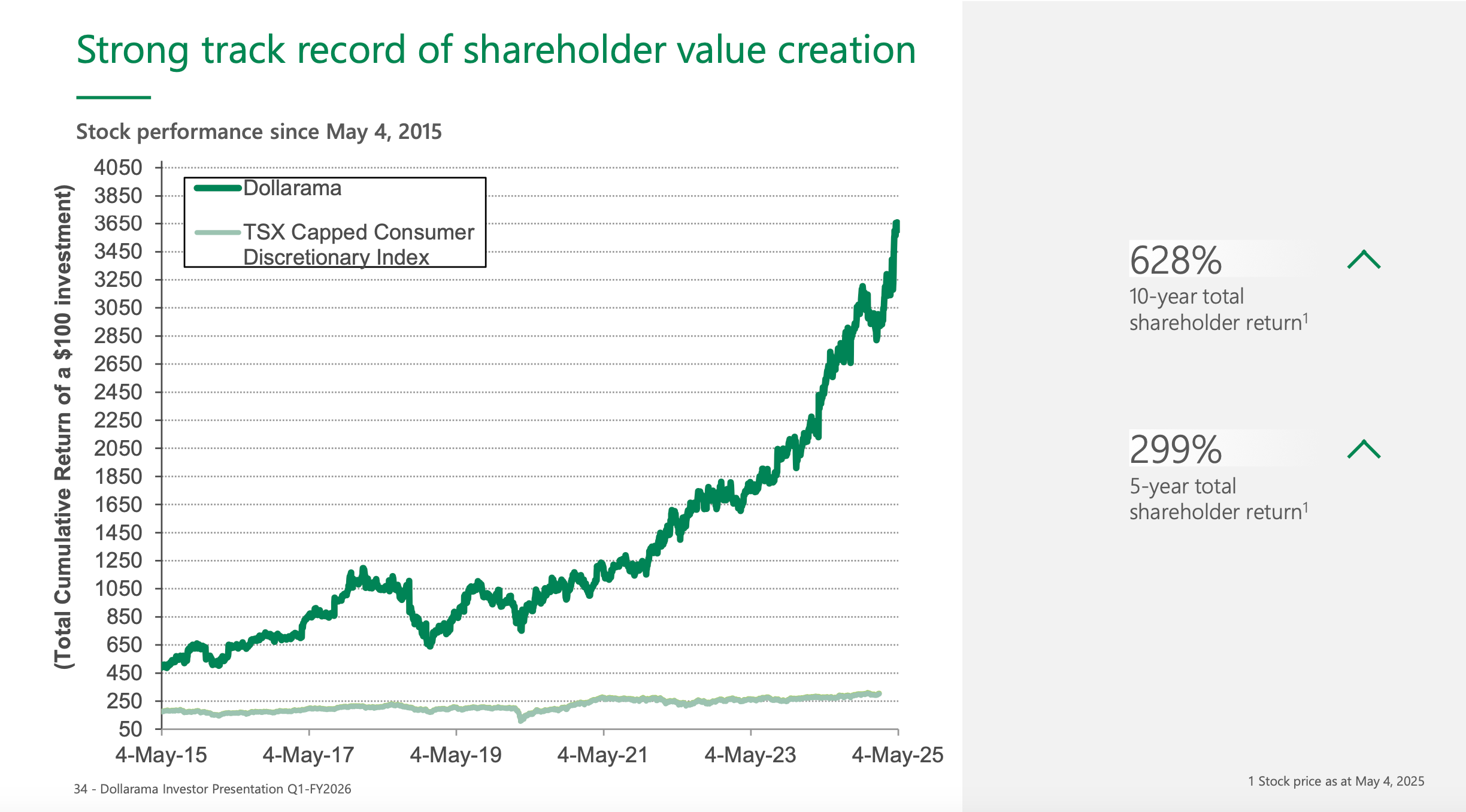

Over the years and decades, there have been very few retailers that shot the lights out in terms of above-average performance. The Canadian Dollarama serves as an excellent example. The stock hit a new all-time high today after the company’s multi-year flywheel showed no signs of cooling. So far, we’ve greatly regretted not buying into this one on late December 2023; our limit order didn’t get hit (missed it by a few pennies).

Last year, the company increased its stake in Dollarcity at what we believed a full price, but hey: that Latin-American growth story seems to have been worth paying up for. We’ll definitely publish a write-up on Dollarama at some point, because there’s so much to learn from such atypical outperformers.

Another area that’s been atypical is the sauna market, as we’ve reminded investors of earlier this week when we pitched Harvia to a Belgian family office.

If Harvia didn’t exist or wasn’t publicly listed, there would have been no chance we’d sought exposure to the sauna and spa market. Its nearest competitors have EBIT margins of 0-5% at best, and don’t have an incentive to grow their market share (they can, but it would be very unprofitable for their owners relative to paying themselves dividends and reinvesting these into the stock market (that’s what ROIIC is all about).

Notwithstanding that the sauna market as a whole is growing nicely, it’s fair to say that virtually all real economic value (and thus shareholder value) generated has been driven by Harvia. Its stock produced a 5-year CAGR of 37% when other COVID winners have yielded real negative (or close to) returns.

As a result, identifying excellent compounders starts with one overlooked factor: luck. Being fortunate to have come across the name of such company and the fact that it’s publicly traded.

4️⃣ Changing Your Mind

Investors shouldn’t be anchored to past opinions, nor should they refrain from getting back in at perhaps higher share prices if the overall investment case 1) looks more compelling versus at the time of your prior ownership, and 2) results in a forward return that meets your criteria (also adjusted for risk of permanent capital loss or a simple multi-year period when it’s turned out to be dead money).

What's the best example of seller's remorse? Probably Procter & Gamble, which I just bought back recently. We sold it because we thought it was a company that was addicted to price increases as a way of growing revenue. And just after we did so, Nelson Peltz went on the board. And I don't know what he said to them or did to them, but they somehow seem to have worked out that you need to sell more of stuff as well. And good. So, I bought it back. I mean, I think the simplest thing to do when you've something wrong like that is, well, correct it, change your mind. - Terry Smith

The same’s true for averaging up: if the business has outperformed your expectations and should continue to deliver sustainably solid results, then adding more likely makes a lot of sense.

Terry’s point on price increases and/or inflation is a very valid one that’s distorted ROIICs, profitability, short-term stock price returns where investors had simply paid up for too rosy expectations. It’s one of our main concerns for industrial serial acquirers: for the most part, incoming acquisitions’ ROIIC won’t be close to that of the prior 5-year period. It seems that investors expectations haven’t so far adjusted for this development.

5️⃣ Management Honesty: Adjusted Numbers vs. Underlying Performance

This quote from Smith is absolutely fundamental to assessing management teams’ honesty/integrity, and frankly, our own performance as well.

Adjustments. I touched upon it in relation to management's presentation, right? An awful lot of people now put out, quote, adjusted numbers.

And I know you're going to find this difficult to believe, but the thing that they take out to adjust the numbers is usually the bad bits. And so, you know, you look at these numbers and it has a little asterisk. And down at the bottom, in much smaller print, it says, you know, removing, you know, amortisation of goodwill, restructuring costs, litigation costs, et cetera, et cetera.

The more adjustments there are, the worse that they're conducting themselves. You know, one of the people that we really liked as an investor in one of the companies we invested in over the years is L'Oreal and Jean-Paul Aigon, who was the CEO. And I particularly remember, they were struggling with, I think it was Brazil, and as a, quite a big market.

And he was asked in the Q&A session by one of the analysts, what would the numbers be like if you took Brazil or Latin America out? And he said, well, obviously, it would look better, but what would be the point of that? I love it. Yes. If you take the bad stuff out, it always looks better.

If we also adjust for what we consider to be one-time headwinds (which then also impact our view on ROIIC), there’s a risk of effectively lowering our bar for letting truly excellent companies earn a spot in our high-quality growth portfolio.

6️⃣ Tangibles versus. Intangible Assets

This part of the interview is most intriguing. On the one hand, we want to own companies with high returns on incremental invested capital.

On the other hand, these are then mostly found in very capital-light sectors, or when there’s unnoticed distortion around leasing (showing a fraction of the underlying asset value that’s being used to run the business operations) or outsourcing (letting someone else produce the products for you, i.e., the assets aren’t shown on your balance sheet).

It's tangible. And it's got some interesting characteristics.

One of them is they're relatively easy to replicate with money. Just go out there. And not only that, you can usually borrow the money to replicate it.

So, if you want to build another shopping centre, or buy another fleet of vehicles, or build some factory equipment, usually your bank will look at its tangible value and feel comforted by that, rather stupidly in my view, but it doesn't matter. I mean, I was in banking myself. What they should really call is pawnbroking.

You can borrow quite a lot of money to finance your investment in those assets, which makes them easy to replicate. And not only that, the very fact that you can borrow money drives the expected return down towards the cost of debt.

Versus intangibles.

If we're in the business of installing glyphs or veterinary testing equipment or mass spectrometer equipment for analysing drugs and food, we've got a tame market to sell things into people.

Yeah, it's a physical asset, but it's got an intangible value in terms of having a client base which is pretty tame and secure and locked into it over time. The other thing is, properly maintained intangibles can last forever. In terms of valuing companies, one of the commonest mistakes that's not discussed much is time.

So, one of my trick questions for people is always, we buy an asset – I don't know what it is, a cement mixer, right? – and we pay 100 and the return every year is 20. Is that a good or a bad investment? Well, over time it turns into a very good investment. How long does it last is the question you've got to ask.

Because if it lasts four years, it's a really lousy investment. If it lasts 20 years, it's a really good investment. It's the same with assets.

Of course, capital-light sectors attract competition, and companies are being replaced faster than ever (as discussed in the blog on McKinsey’s valuation book). It’s all about longevity and optimizing the business for continued success.

For Constellation Software, churn has been fairly low (as is to be expected given that we’re talking about specific software), with the average client relationship spanning 25 years (or longer).

Linde’s long-term supply contracts and contractual project backlog ensure a minimum return on investment.

We think it was late 2019, when Harvia’s CEO touched on the continuous focus on productivity in its facilities; and even during the 2024 CMD, they said that the Muurame factory had still room for improvement.

Our good friend and highly appreciated member

(who documents his learnings and research on Substack too!) mentioned Norbit as great example of focusing rigorously on improving production efficiency and staying close to engineers for improved product quality.

We’d say the one thing that worries us most about pure intangible businesses and high cash flows/ROIICs: managers can become complacent and think they can do whatever they want; just because many of the investments aren't reflected on the balance sheet.

If you invest in sales and marketing expenses, it’s directly subtracted from your gross profit. It’s not capitalized, and hence, it’s not being added to your invested capital number. How can you then gauge the effectiveness of capital allocation? When multiple initiatives fail and drag down your bottom line for several years, it becomes difficult to pinpoint the inflection point where growth spending starts driving incremental sales and real profits.

If you invested in a new plant or machinery, and it doesn't work out for the next decade, the market will easily figure it out via your CAPEX spend and the related growth in NOPAT. It’s all being registered on your balance sheet (and you can work out the historical cost (before any depreciation) too; same’s true for divestiments). Understanding the pay-off on investments in brand equity and/or acquiring market share is a lot more ambiguous.

In Q4 2024, Harvia made strategic investments in sales and marketing around the holiday season in the US to enhance its brand awareness. As a result, EBIT and FCF margins dipped (on purpose). As we wrote in February:

The decision to accelerate market share gains yielded a 0.7 million EUR in incremental steady-state NOPAT in just one quarter. That’s a 46.7% ROI on growth SG&A… Having a high ROIIC on regular CAPEX as well as flexing the SG&A muscle is what keeps the flywheel going.

In Q1 2025, overall EBIT profitability recovered strongly, and the highest-ever Q1 sales level was accompanied by a record gross margin. This strong increase in gross profit euros/dollars allows for future strategic reinvestments in commercial support, digital presence, product innovation, and tangible capital investments in new capacity.

For us, it’s easier to identify ROIIC and longevity when there’s a combination of tangible assets (production facilities, distribution network) and intangible assets that support a long-lasting competitive advantage. If that’s the case, a healthy reinvestment rate, excellent balance sheet, and alignment of interest/right incentivization will drive outperformance that’s set to compound strongly over the years. Oftentimes, that outperformance will exceed even the wildest expectations.

This is outstanding! 🙏

Great article!