Terry Smith's Radical Strategy Shift

More about preserving AUM than anything else? Or has he just rung the bell for quality growth to bottom?

As you might be very well aware, Terry Smith published his 1H Letter, and on Fintwit, criticism reigned.

It’s especially remarkable after his interview with Stephen Clapham, when he stated somebody would have to surrender to the market pressure to mark the end of today’s underperformance in (traditional) quality stocks. Smith went on and said: “My vote is it should be Nick (that’s Nick Train from Finsbury Growth and Income Trust).

As you note from the above, Fundsmith’s still in the process of changing its portfolio.

More About Corporate Survival Than Anything Else

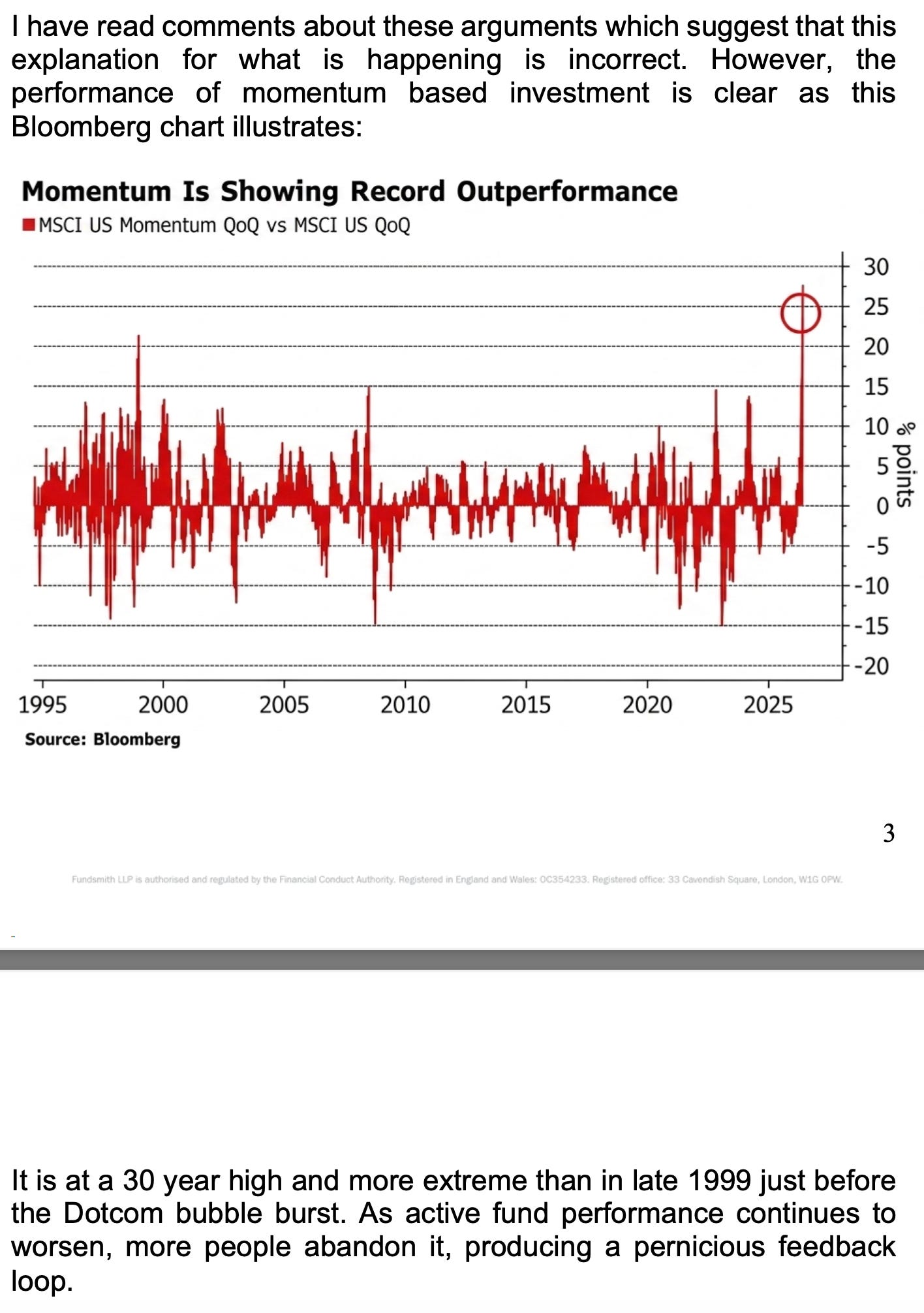

For over a decade, Smith lectured the market on the virtues of low turnover and compounding. But Terry Smith himself decided that sticking strictly to that approach meant risking the adage that “the market can remain illogical longer than we can remain in business.” Critics are calling this sudden high-turnover pivot a clear capitulation to short-term market pressure. They point out that changing a core philosophy right when underperformance bottoms out is classic retail-investor behavior, not the action of a legendary veteran.

In the letter, Terry argued that the market is currently illogical, dominated by a passive index momentum feedback loop rather than fundamental business quality. The general observation is that active managers love to take credit for the market when they are winning, but blame structural market "glitches" and index providers when they lose.

For Smith, a drop from 29 billion GBP to 12 billion GBP (assets under management) isn’t just a blow to the ego. It’s a structural loss of the firm’s revenue. When a business faces an existential threat, the corporate survival instinct always exceeds the importance of maintaining investment purity. The investors who stayed specifically for Smith’s “Buy good companies, don’t overpay, do nothing” mantra are left holding a portfolio they never signed up for.

Momentum-Driven Strategy

In his 1H Letter, Terry blamed momentum investing for the recent years’ underperformance but he’s now started to feel the pinch to be a lot more active as well.

Smith’s recent portfolio changes reflect more exposure to AI, even though he sold out of some indirect AI beneficiaries such as Otis (which was one of our underweight positions, and then we added substantially after its Q1 release).

Data centers require Otis’ infrastructure, and after a couple of softer years for New Equipment, momentum should be picking up. Thanks to improved working capital trends, this drives incremental free cash flow, allowing for substantial buybacks at what we believe to be a low-teens percent IRR. However, as we’ve mentioned previously, we need accelerating growth. Without this, it’s hard to justify a position over the longer run. Meanwhile, Smith held onto Kone and Otis when growth was decelerating at a time of historically high valuations…

FCF Yield is Up for Debate

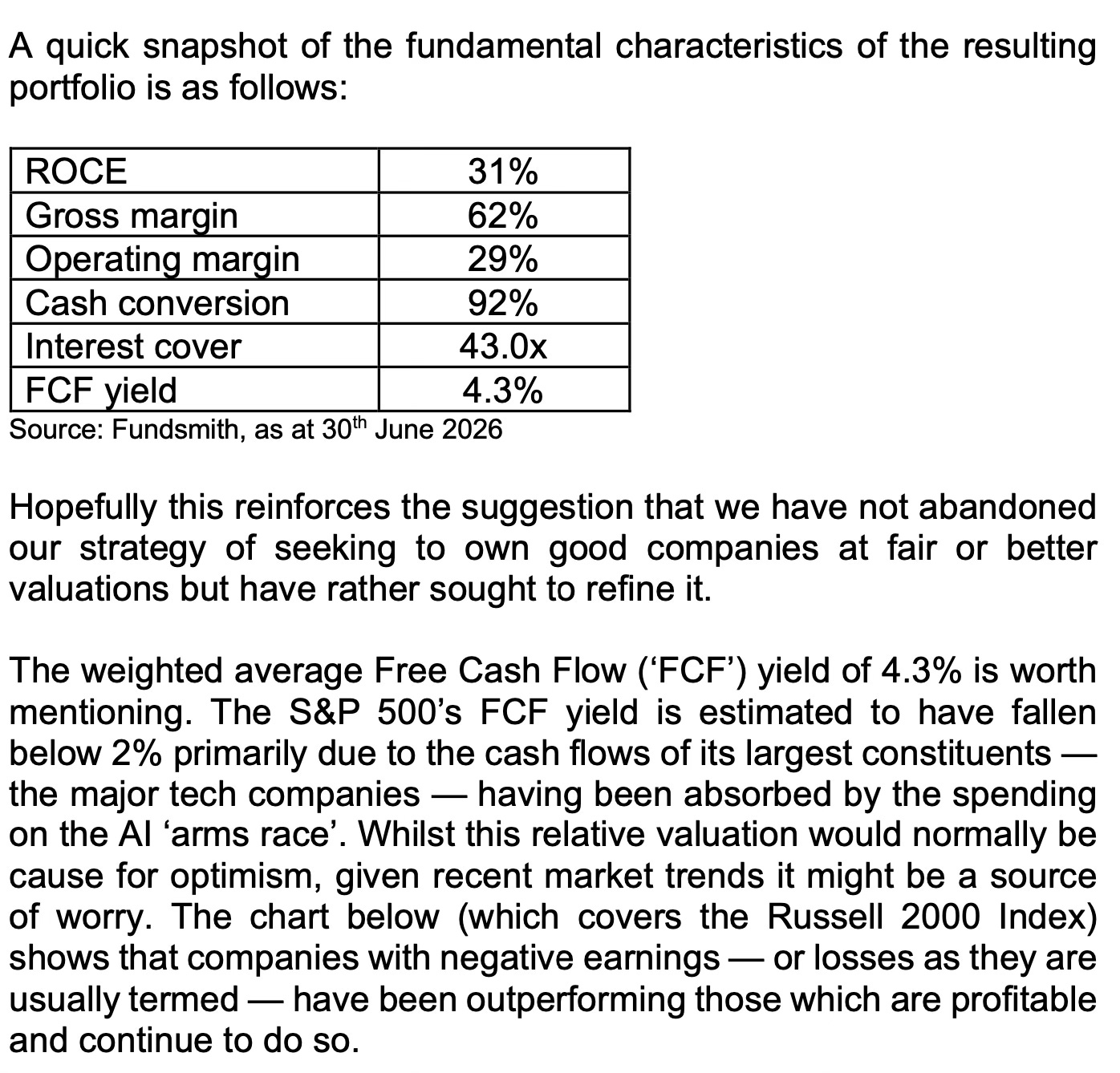

Another element that remains nuanced is Fundsmith’s FCF yield. What’s driving it, and contrary to popular opinion, FCF after all growth spend is not a good proxy to measure the year-over-year growth. FCF’s also impacted by financing costs (or interest income).

The dream of the quality growth investor is a low FCF (after M&A) and high ROIIC, as it implies a high reinvestment rate translating into strong NOPAT growth.

When we published our write-up on Lotus Bakeries, we got the question: is that projected CAGR of 20% in FCF real when NOPAT would be growing at 11-12%. It’s all about the baseline. Lotus’ FCF has been relatively depressed due to a temporarily high CAPEX cycle… So, focus on NOPAT and what’s driving it, and how the company’s investing for growth.

Durability of Returns

While many quality investors who’ve underperformed the market blame it on the AI boom and passive investing trends, there’s also a very straightforward answer to the quite disappointing returns: starting valuation being too high and the lack of growth. Smith’s portfolio has or had quite a bit of names with low growth and a low FCF yield. Something does not add up here, especially as these companies were not reinvesting a lot into growth (maybe some M&A, which means that the spend falls outside FCF still).

The best part about the broader derating is that several pockets of quality growth continue to show good growth (say 12-15% per annum) but because of the labeling investors may not always make a clear distinction between what’s reasonably valued and what’s not. Pretty much anything with a quality label has faced multiple contraction but we continue to believe in case-by-case analysis.

Terry Smith’s Track Record & Timing of Returns

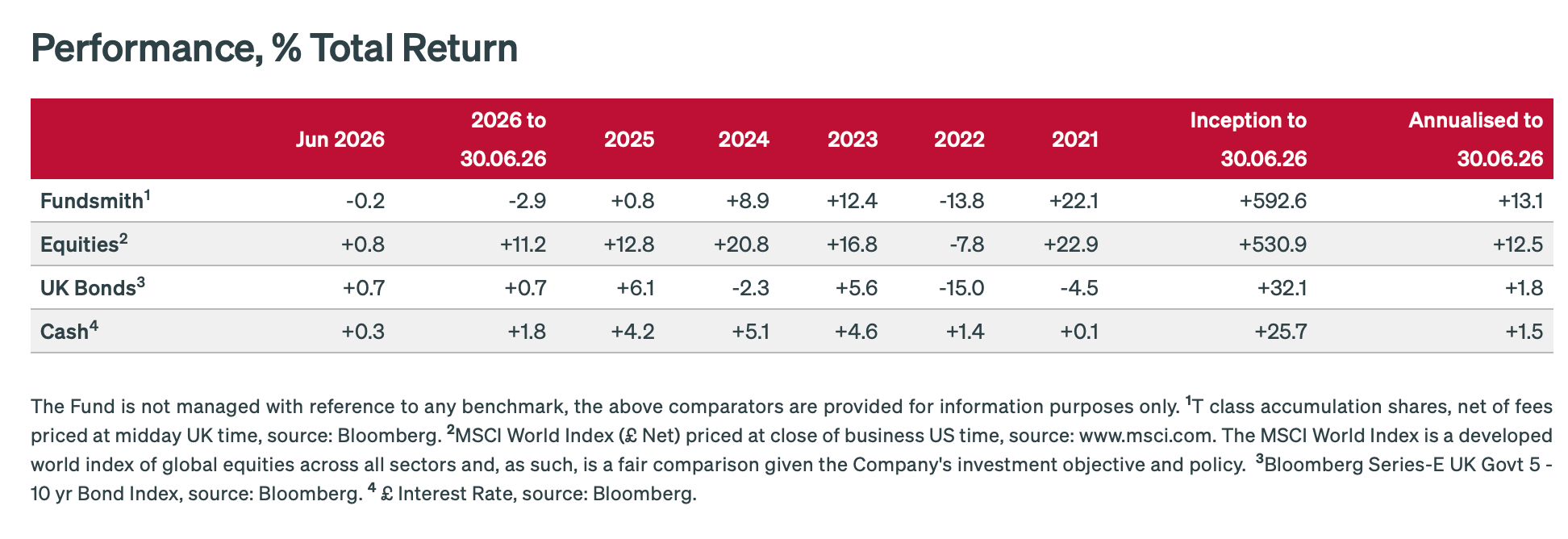

Despite the recent years’ underperformance, Terry’s outperformed the index since the Fund’s inception but there’s some nuance to that.

All the big wins happened early on when the fund was small, and the losses kicked in later after the fund grew. Because of this, the money-weighted CAGR, that is the actual returns investors took home, likely shows heavy underperformance. It's a very common problem in the industry, also reflecting momentum: seeing evidence of a strategy working well/beating market is attracting attention.

We’ve already brought it up: investing is a continuous process, and even though the sequence of returns does not have an impact on a portfolio with a fixed starting base, dynamic flows are relevant. Investors will be adding money to their account, withdrawing (reaping the benefits during say retirement), maybe very frequently.

Hence, we want to own a portfolio that’s not getting too much ahead of itself when we’re still in the phase of adding capital. It’s not helpful to new subscribers either.

If our portfolio would have CAGR’ed at 30% over the past two and a half years on the back of 14%-15% growth in underlying earnings per share (EBITA, the pre-tax NOPAT), how would we feel about this? Very nice to have that kind of a 2.5-year track record but knowing that half of the CAGR came from multiple expansion, it doesn’t reflect the recurring nature of that CAGR to be sustained over time.

Long story short, we repeat what we’ve stated in our 1H (and previous) Letter:

As stated previously, we focus solely on underlying earnings growth, making sure it’s being driven by company-specific execution. It’s tough to predict valuations but over time (a 7-10-year view), 80% of our success should be driven by the compounding in NOPAT per share. While today’s valuations are very reasonable, it’s up in the air whether and when we might reap the benefits from a re-rating. We know we cannot predict such turnarounds (be it favorable or unfavorable). For us, it’s simple, and there’s no way to hide the outcome. If we don’t get a low-teens or better percent growth in NOPAT/share (portfolio-weighted) and fail to maintain turnover at a low level, performance will not meet our expectations over the long run. Growth at high returns is our strategy’s north star as it eliminates our focus on getting valuation right

This is especially true as we’re not significantly exposed to industries or companies prone to disruption or fancy technology. One can definitely make good money being more active but it’s not a skill we possess; we’re quite happy with our own approach as we seek and earn competitive and durable growth in earnings at high ROIICs.

All while maintaining low turnover when fundamental compounding is working out as planned. There’s no need to change a winning team. Think of it as being a private business owner. If you owned a private business with steady, grinding profit growth, you wouldn't sell it every quarter just because competitors are fetching higher valuation multiples.

Our Take - We’re Managing Our Own Money, and The Portfolio’s Attractively Priced with Accelerating Growth Momentum and 30% ROIIC

Contrary to Smith, we’re not making a radical change to our strategy. We’re managing our own money, and by now, we hope we’ve attracted like-minded investors. Thus far, we’ve got clear evidence of owning the right companies, and we’ve seen accelerated growth momentum that’s down to company-specific execution.

As long as our managers keep their full focus on the business and allocating capital wisely instead of the share price and related volatility, we’ll be in very good spot. That does not mean it’ll be easy for investors to sit tight. There is notable volatility, and it’s increasingly driven by technical rather than company-specific factors. Rebalancing or just tight share ownership. For example, a less liquid stock can show some significant price swings during the Summer months.

We do believe today’s growth rates of 14-15% will eventually moderate toward 11-12% over time as more uncertainties and challenges on the reinvestment runway arise but thanks to a 30% ROIIC (not just ROIC but the incremental returns), our companies don’t have to reinvest an awful lot into growth to yield a satisfying outcome.

That’s another topic we’ve addressed in our 1H Letter: expectations management - why would company X be able to grow at a given rate? What are the hurdles? It’s one thing to find good companies and extrapolate the past successes, it’s another to be realistic on what to expect and spot opportunities when the market’s not paying attention.