Optimizing the Risk-Adjusted Performance of a Quality Portfolio

Introductory Course to "Portfolio Overwriting"

Last week, we conducted a poll to gauge interest in an introductory course on "Portfolio Overwriting" as an add-on/byproduct of our approach. There was significant interest, both from those eager to learn and those looking to apply the knowledge in practice.

For any strategy, one should be able to elaborate on the puts and takes: what to expect, what’s the performance during bear markets, bull markets, how random are the returns, et cetera. Testing statistical robustness and keeping real-life consequences (taxes, transaction fees because of portfolio turnover) in mind, rather than taking the average return for granted, and hoping for a similarly good outcome over the next years.

What’s the benefit of selling calls on a basket of defensive, lower-volatility, high-quality companies (think of your Colgate, Procter & Gamble, McDonald’s, Danaher, PepsiCo, Linde)? The fact that we’re talking about stable compounders is crucial: everything starts with the right underlying on which you sell the call option.

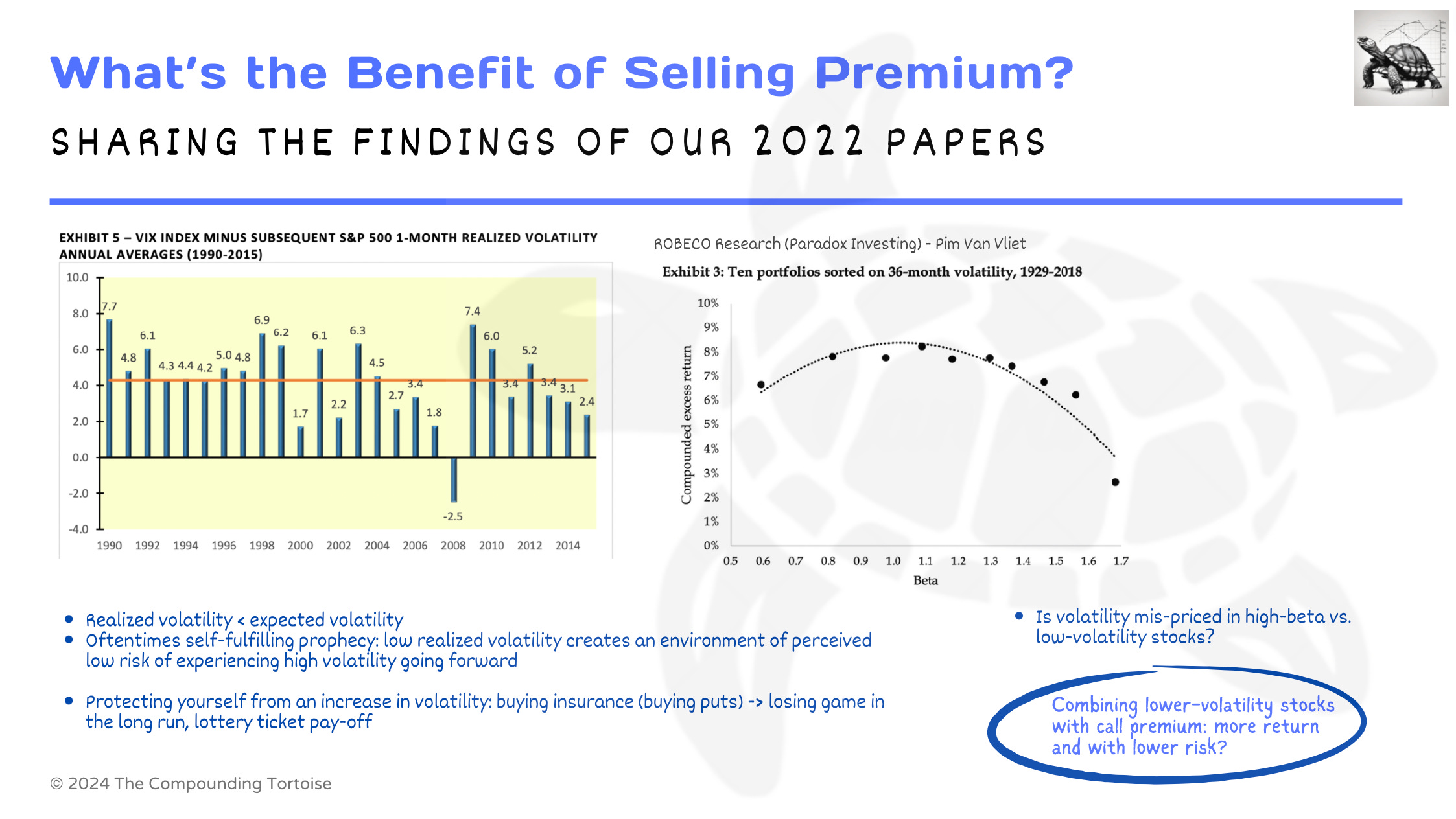

In the below video, we share the basics of portfolio overwriting (i.e. longer-term covered-call writing) and the findings of our 2022 papers (>20 years backtest).

What we’ve been talking about previously: low-volatility, quality factors outperforming the index and high-beta low-quality stocks is reflected in the options market. Longer term, options premiums for steady compounders are relatively rich compared to their actual volatility.