Introduction

Back in February, we wrote an article on why Return On Invested Capital can be a flawed metric (especially when there’s more inflation, when you’re dealing with companies that do some one-off growth investments).

Rather than saying: look for high-ROIC companies and you’ll be fine, we argue that there’s a lot of hidden value in picking those that have a strong ROIC (our hurdle is >25%) and whose competition does not. “Moaty” sectors are not necessarily the best places to look for steady outperformance throughout the whole cycle (just look at tech in the 2022 bear market despite generally favorable margin characteristics, capital-light business models and growth prospects).

When you’re able to achieve an ROIC that’s double or even triple your next close-in competitor’s, you’re doing something special: you possess some unique characteristics that will enable you to accelerate shareholder value creation when reinvesting cash flows back into the business (CAPEX). We’ve touched upon this already in a previous article.

In fact, as we look at our portfolio, our companies really stand out in what many would perceive to be boring industries. Sustaining that high ROIC while reinvesting for future growth is what creates a barrier that’s very difficult to overcome for new market entrants. The best part about it? Our companies’ outperformance has tended to grow during periods of higher inflation and low economic growth, i.e. stagflation. That’s when you need truly amazing compounders!

Let’s highlight three case studies and portfolio holdings that capitalize on their outstanding ROIC, ROIIC, balance sheet and consistent reinvestment rates. We’ll be covering more of this in the upcoming bi-weekly webinar.

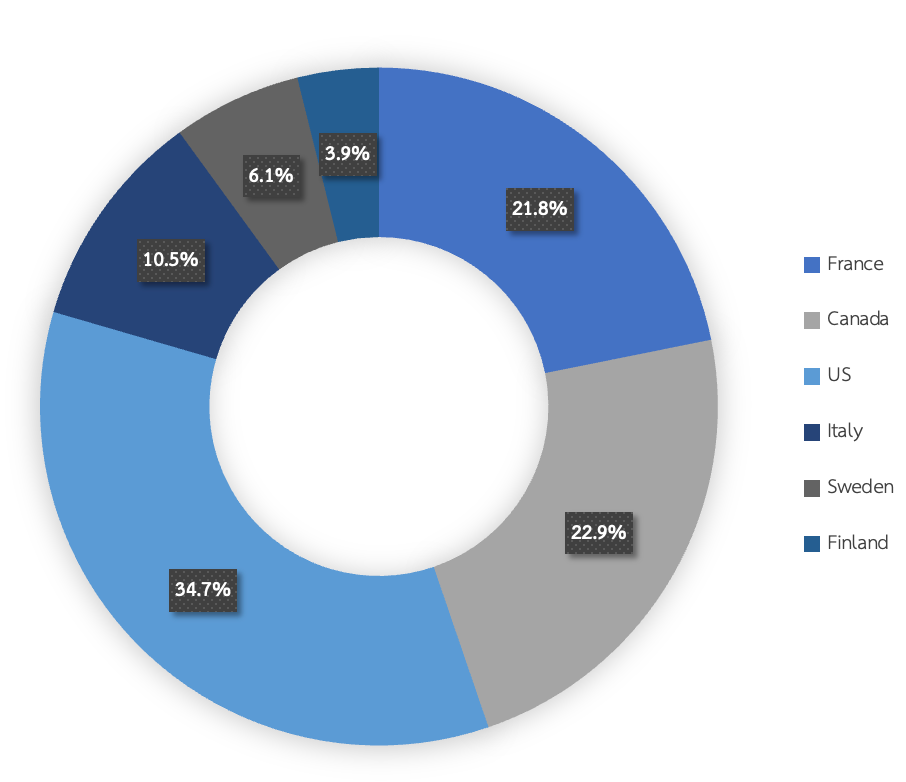

Here’s our portfolio breakdown by country of listing.