The Committed Shareholders During Times of Passive Investing

"Building great companies with short-term investors is a challenging mission"

This is a bit of a follow-up on last weekend’s video update; and partly a news digest as we’ve received increasingly more questions on what’s going with Constellation Software. We’ll share three growth-valuation scenarios; no predictions - just running the numbers objectively.

Yesterday, we stumbled on a very interesting book written by Sarah Keohane Williamson. She’s the CEO of FCLTGlobal, a nonprofit coalition of global pension funds, sovereign wealth funds, asset managers, private equity firms, and major corporations. You can order the book ‘The CEO’s Guide to the Investment Galaxy” on Amazon (our copy will be delivered early February).

FCLTGlobal

We have previously emphasized the significance of a company's shareholder base, a point that rings especially true today as several high-quality stocks have taken a beating, even those once thought to have the most loyal investors. Now, we can back this up with third-party reading material.

Just an introduction on how Williamson views the concept of long-termism vs. short-termism in a recent interview with McKinsey’s Tim Koller.

Who’s Backing You?

It’s evident that you can’t (and really shouldn’t) please every investor. You’ve got investors with different time horizons, different profiles, different set of expectations… Also, people who’re misinformed about your business (e.g., like we’re seeing the wrong valuation metrics being quoted for Constellation Software).

This variety is actually a benefit; it lets long-term investors profit when the market misprices a stock based on short-term trends rather than future growth and ROIIC. If management continues to look out for serious, long-term shareholders, patient investors have a great chance to outperform.

CEOs tend to believe their shareholders are “on their team” and that they want their company to succeed over time. Unfortunately, it’s not quite that simple. Some shareholders are retail shareholders, and so they probably are on the company’s team, in that they just want to see the stock go up. But then there are index managers, who tend to own shares in a majority of companies. They might want the company to do well, but they might want their competitors to do well, too. And then there are active managers. If they’re overweight, maybe they really do want the company to succeed. But maybe they’re underweight, which means they don’t want the company to succeed. These are the sort of things that drive CEOs crazy because it’s unclear who’s really rooting for them and who’s not.

We don’t want to make this sound romantic like “Long live long-term ownership, just close your eyes and you’ll be fine”. What we said declared was also called out by Williamson.

What matters to the real economy is not so much the stock price or its volatility. It’s how management reacts to it.

If the management team falls victim to the share price woes (whether it’d be euphoric or pessimistic), they’re going to make mistakes which tend to be irreversible if you’re dealing with an over-levered situation and low ROI(I)Cs.

Unrealistic expectations inevitably collide with reality: high growth eventually moderates. This decay is a primary reason why high-beta stocks generally underperform on both an absolute and risk-adjusted basis, if you’re holding them for a longer period of time. There are investors who can time their exit perfectly, but there’s usually other players who’ve lost a huge chunk of their invested capital.

The pattern is driven by a consistent trait of human behavior: as momentum accelerates, investors rush to chase the parabolic move. By increasing their stakes at the top, peak volume on the way up usually serves as a marker for peak optimism, and the subsequent impending reversal. When using options on these stocks, it’s oftentimes a zero sum game.

Crafting the Right Shareholder Base

The following quote seems too focused on the intrinsic value component of investing but it’s the only thing that matters. Share prices are a consequence of management actions over the long run. Pumping your company’s valuation/expectations doesn’t benefit society - those who buy the overvalued shares will be left a poor or negative return.

The first step is encouraging long-term investors. The second is not playing into the hands of the short-term ones. The latter requires the classic things: Don’t give quarterly guidance, don’t do the things that really attract short-term investors, which is, of course, because they’re trading. The other thing is, frankly, don’t listen to them.

Analysts Vs. Shareholders

The following is related to the above: focus on the shareholders you should value most.

You have to remember that the sell side is, by definition, not a shareholder. When I hear, “Our investors think such and such,” I ask: “Are you talking about an investor or a sell-side analyst?” The book refers to sell-side analysts as weather forecasters, which is not meant to be derogatory. Weather forecasters take in all the available data and try to predict the future. That’s what the sell side does. But they’re not shareholders, and every company, every CEO, every board has a fiduciary duty to their shareholders. They do not have a fiduciary duty to the sell side or the financial press.

Providing Guidance

Sharing guidance can give investors a false sense of precision or an anker to focus heavily on the near-term outlook. Rather, companies should provide colour on the puts and takes when setting expectations (e.g., seasonality in a given quarter, timing of deliveries impacting sales). Rather than offering a quantified outlook, managers should focus on contextualizing quarterly results and sharing the longer-term roadmap (e.g., annual sales growth, a minimum level for EBIT(A) margin, leverage (to prevent chasing growth through acquisitions at unattractive IRRs).

The reason that guidance about future earnings is a detrimental practice is that if I say, “Next quarter, we’re going to earn $1.27 to $1.30,” and then it looks like we’re not, human nature makes company leaders think, “Uh-oh. I’ve promised that we’re going to do this, so I’m going to do something to make it happen.” Companies inevitably do something on the revenue or the cost side to hit the number. If they do that again and again, they’ve gotten themselves on this short-term track. The best thing to do is to have a long-term road map—let the street say what they’re going to say, report the numbers as they are, and talk about what you’re trying to accomplish over time.

Constellation Software - The Share Price Drop Continues

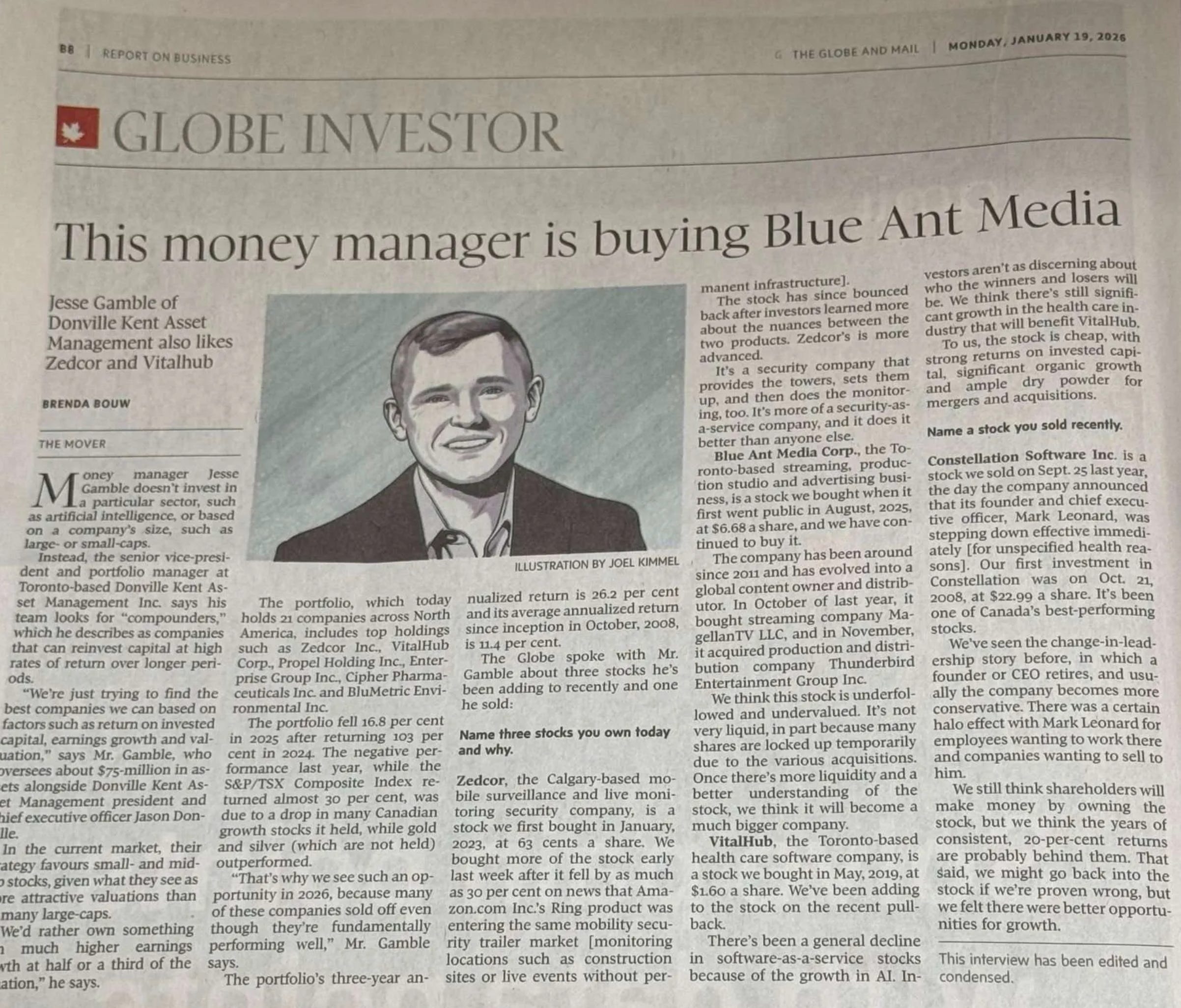

It’s now the most-debated stock on our Discord channel - CSI shares have continued to slump, marking at drawdown of around 48% in about six months. It’s unprecedented. Last Monday, the Globe and Mail came out with this article, highlighting the recent move from Jesse Gamble at Donville Kent AM. They sold their CSI position last September.

It is perfectly reasonable to believe you can outperform CSI’s expected returns by redeploying capital elsewhere. Ultimately, that is a personal assessment of risk and reward. Investing is a perpetual exercise in opportunity cost—the constant weighing of whether to hold a current position or swap it for a more promising alternative, often followed by the hindsight of “I should have done X or Y.”

When stock prices experience elevated volatility, pinpointing a single cause is difficult. However, in a market increasingly dominated by passive flows, the risk of “committed” shareholders stepping away has risen. It somehow reminded us of this compiled interview with Chris Mayer and Bogumil Baranowski.

That’s clear because passive investing isn’t committed as one would think: it’s easy to sell an ETF versus checking upon your positions individually. And still, there must be strong alignment to not sell for whatever reason. Mayer talked about Woodlock House Capital and why it’s required to not just take anybody’s money.

If you have someone who’s not aligned with that, then they’re questioning you all the time, makes for unpleasant experience, and affects the returns of the partnership.

Even the most stellar track record offers little comfort when short-term performance lags. We can see this play out even in passive vehicles - when investor expectations become decoupled from reality and earnings growth inevitably moderates, a ‘dead-money’ period will be difficult to handle for most investors as they haven’t lived through a meltdown or sideways market before. Markets have a way of correcting exuberance over time, and major index companies aren’t inherently low risk, especially not at times of heightened concentration. While the ultimate goal remains an adequate return on capital, the modern investor has become hyper-focused on instant gratification, losing the sense of what drives long-term value creation.

We steadfastly believe that CSI has historically generated immense wealth precisely because of its sticky shareholder base. When a company compounds capital at such high rates, there is little incentive to exit; especially when management’s “quiet” approach (avoiding quarterly calls and granular guidance) discourages short-term speculators. This culture has served CSI well, as they remain among the world’s elite capital allocators, a fact evidenced by their consistent incremental returns on capital and the scale of their deployment.

Currently, many high-quality funds are facing sizable redemptions, forcing them to liquidate positions and putting downward pressure on share prices. Furthermore, with the prevailing AI narrative casting a shadow over the broader software sector, CSI’s long-term outperformance creates a psychological trap: loss aversion bias. For many managers, selling a winner like CSI to lock in a profit feels significantly better than realized losses on a “big loser”, even if the long-term fundamentals suggest otherwise.

We also believe that there’s misinformation on CSI’s valuation - not making the distinction between the fully versus proportionally consolidated numbers. Not adjusting for the non-controlling interests in Topicus and Lumine leads to a 15% higher EBITA (and NOPAT) in FY25 - a percentage that’s expected to grow as the spins should outgrow the mothership. Anyone who’s quoting EV/EBITDA, FCF (not FCFA2S)… should bear in mind that this valuation metric is not comparable to the pre-2021 situation (when CSI spun off Topicus) - it’ll be too low on an unadjusted basis. When you’ve got investors on board who can’t interpret the numbers, it’s going to pose a problem during volatile times.

The pivotal question now is: what do forward returns look like under various capital deployment scenarios? Let’s examine our model.