What The Factor?!

Debunking investment return drivers & relative performance

Introduction

As quality growth investors, we primarily seek to effectively capture the so-called quality factor premium. We’ve already elaborated on the reasons why quality growth companies outperform over the long run.

Some quality growth stocks exhibit strong long-term momentum, below-average volatility, and good relative value. To put another way, they combine several characteristics that should produce solid long-term returns, i.e. factor investing.

Factor investing can be traced back to the 1970s. Investing in market segments with features (factors) that have historically produced higher risk-adjusted returns than a passive investment in the market portfolio is known as factor investing.

In order for such feature to be called a “factor”, it has to meet the following five criteria:

Performing: show strong premium with superior risk-adjusted returns;

Proven: surmounted attempts for falsification;

Persistent: observable in different markets, stable over time, robust to different definitions;

Explainable: have an economic rationale with strong academic underpinnings;

Executable: implementable in practice; e.g. survive after trading costs and other market frictions.

Factor premiums (as they’re generating a return in excess of the market’s) are anomalies to the Capital Asset Pricing Model (CAPM). The CAPM is a theoretical pricing model introduced in the early 1960s and assumes a positive linear relationship between the systematic risk and the expected return of a stock or a bond.

ROBECO

Four generic factors are value, momentum, quality and low-volatility. Factors are very nuanced, which makes it more difficult to figure out which factor has been or will be the main return generator for one’s portfolio.

Value: buying stocks that are trading a low multiples (earnings, cash flow, book value…). Prominent academics, such as Eugene Fama and Kenneth French, have argued that the value premium is a compensation for risk, in particular distress risk. However, this may not necessarily be the case. There’s no empirical evidence that distress risk drives the value premium has been reported so far.

In our portfolio, we look at value from an IRR perspective. If we can earn our absolute return goal with a stock trading at 20x EV/NOPAT, we’ll buy it. At the same time, this stock isn’t likely to make the cut in a traditional value investor’s framework. Growth in cash flow, ROIIC, reinvestment rate is an intricate part to valuing companies. Buying compounders and holding onto them for a long period of time is effectively de-risking the fair or seemingly high multiple you paid initially. In other words, we don’t follow the rationale of looking at lowly rated stocks.

Momentum: The momentum premium is one of the largest factor premiums, but its sensitivity to market reversals and high turnover are two well-known issues that plague the implementation of a momentum strategy. By focusing on stock-specific momentum (relative performance versus the market, corrected for the stock’s beta, rather looking at absolute outperformance), one can optimize the effectiveness of the momentum strategy. Still, what time frame should you use to gauge negative or positive momentum?

ROBECO

Low-volatilty: generic low volatility strategies are typically based on a single backward-looking historical risk measure, such as volatility or beta. This construction, however, may expose the strategy to some pitfalls, such as miscalculated downside risk. Not all low volatility stocks are equal and some are destined to perform better than others. Forward-looking risk measures such as distance-to-default or credit default swap premiums provide an additional layer to the traditional low-volatility factor.

Quality: a key concern with generic quality strategies is that they use poor definitions, which are sometimes even blended with other factors. For example, quality is often measured by financial leverage or earnings stability, which are actually more related to the low volatility factor. Other quality definitions – such as growth in profitability or earnings growth, but

also an oft-used measure like return on equity (ROE) – have weak or no predictive power for future returns. A good definition of quality should be multi-dimensional and incorporate profitability, earnings quality (low accruals) and investments (management policy, i.e. no excessive

issuing of shares by CEOs to expand their emporium). Each of these three themes has strong academic underpinnings and is shown to have a strong stand-alone performance, as well as when combined.

In short, factor investing allows us to benefit from higher absolute and risk-adjusted returns by combining the individual quality, low-volatility, value, momentum factors. Factor investing is part of a series of discussions on our private Discord.

However, factor investing is a long-term story. The past five years have been tough for factor quant strategies whose underperformance (and in most cases negative real return) was driven mainly by the lack of exposure to higher-beta momentum stocks in 2020, 2021, 2023 and 2024.

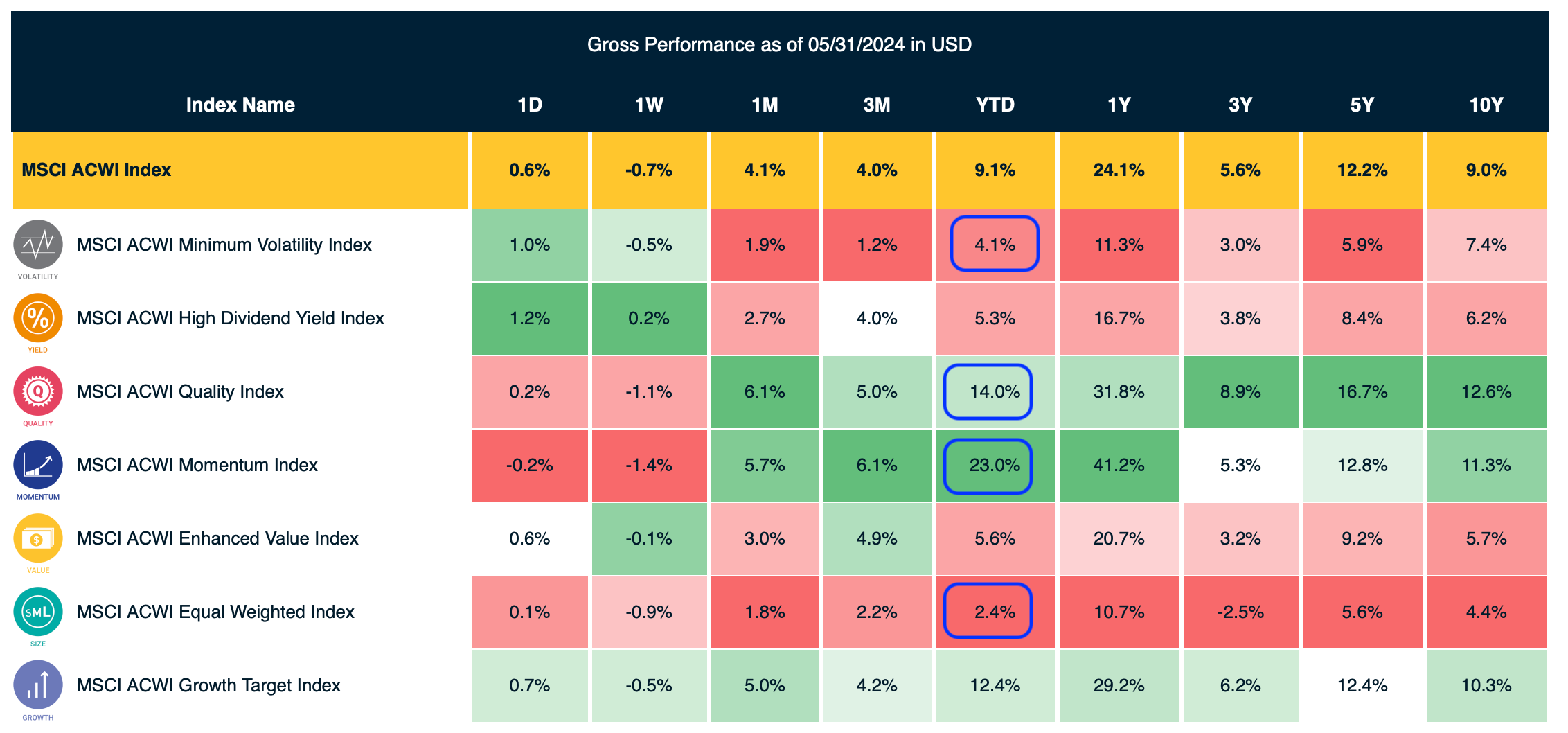

The below table illustrates the performance for the MSCI factors on a global basis. Only momentum, quality, and growth were able to outperform the index on a 5 and even 10-year basis. It shouldn’t come as a surprise to learn what sectors/stocks drove their relative outperformance: technology and the Magnificent Seven.

Year-to-date, minimum-volatility scores worst (similar to last year), while momentum is the place to be (also similar to last year).

Relative performance

Given the wide return dispersions between certain more defensive and more crowd driven factors (momentum, growth), there’s an ever-growing temptation to compare ourselves to the index.

In one of our February 2024 articles, we wrote:

Naturally, human beings want to compare themselves to others. In the world of finance, it’s killing to think you can always beat the market and, in most cases, the market index won’t serve as a good comparator to your individually selected stock portfolio. Suppose the index is down 40%, does outperforming it by 5% make you feel happier? Conversely, will you be disappointed when the market was up 20% and your strategy delivered the targeted 12%?

Also, to beat the market by a very wide margin or to strive for lottery ticket returns, investors turn to more risk-taking (high beta) which does not correspond with a linear return relationship. Taking on excessive risks isn’t priced efficiently. In other words, you could end up feeling lucky with a few high beta stocks, but a whole collection of risky assets will demolish your risk-adjusted performance.

We don’t focus on relative performance for several reasons:

We have our absolute return goal (12% p.a.), which will be driven by our companies’ performance. Over-trading our portfolio because of relative performance would simply result in us making wrong decisions at the worst possible moments.

Our portfolio has a high tracking error: we deviate from the benchmark deliberately. When you’re not holding any of the Magnificent Seven stocks: should you be comparing your performance to the Nasdaq’s or the S&P-500’s? It works both ways: if the Magnificent Seven were to crash, our performance (even it would be negative) would look great. Wouldn’t make much sense to us when we didn’t achieve our absolute return goal.

Are we at an inflection where certain proven styles will make a comeback? We don’t have a crystal ball; it’s difficult to time factor performance and reversals. What we do know is this: increased retail investor participation creates or will create more frequent compelling opportunities, because of 1) their short-term focus on relative performance, and 2) they’re oftentimes positioned at the opposite of the factor spectrum (high-beta, low-quality). Because of this, momentum swings have been more prevalent in today’s market environment. A stock can become in and out of fashion rather quickly.

We expect more volatility and more opportunities to top up the returns (i.e. putting cash to work at very attractive IRRs, high IRRs we shouldn’t get on top-notch quality growth companies that are supposed to be priced efficiently).

Our goal is to maximize the IRR on every purchase we’re going to make throughout our entire investing career. Preserving capital and keeping cash on the sidelines will make us stay the course more easily and capture outsized IRR opportunities (>15% p.a.).

Conclusion

Defensive factors have been lagging the market for a while now. While it’s difficult to break out each factor’s attribution to our portfolio, we firmly believe that steady growth, good valuation (reflected in a solid IRR that balances risk and reward), and consistent cash generation will remain the three key tenets to our overall portfolio strategy.

Short-term momentum is very difficult to trade (especially after taking costs into account) and we believe it’s way more important to keep a much closer eye on long-term earnings, cash flow and ultimately share price momentum.